Venture capital markets rely on an assumption of meritocracy. The belief is that the best ideas, the best teams, and the best opportunities rise to the top through rigorous evaluation. The reality of how most venture firms actually source, screen, and evaluate deals tells a more complicated story, and for investors paying close attention, the gap between assumption and practice is one of the most consequential inefficiencies in private markets today.

I recently spoke with Sharon Vosmek in January 2026, CEO of Astia, about the structural biases embedded in standard venture capital processes and how Astia’s Expert Sift methodology is designed to remove them. What emerged was less a story about inclusion as a goal and more a story about investment process as a competitive advantage.

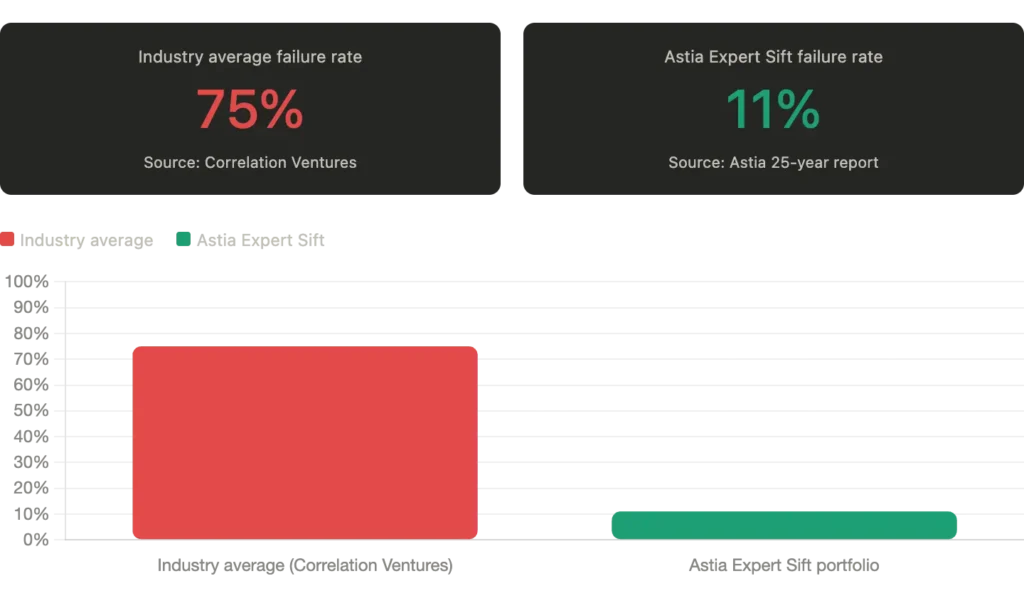

Industry VC failure rate vs. Astia’s Expert Sift failure rate

The warm introduction problem

Most venture firms will not meet with an entrepreneur without a warm introduction. This is presented as a practical filter in a high-volume deal environment. In practice, it functions as a structural gate that favors founders already embedded in elite, predominantly homogenous networks.

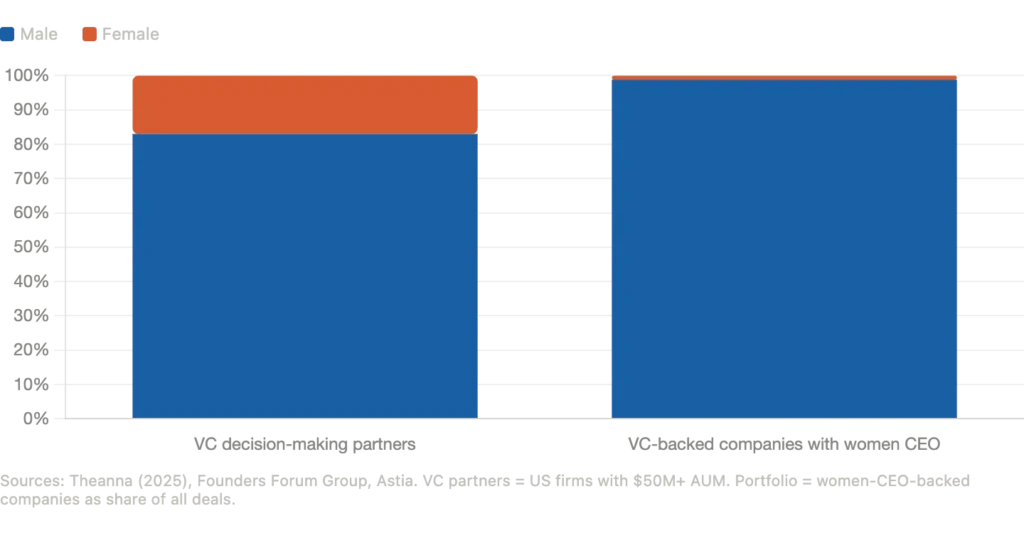

Sharon makes the point precisely: 80% to 90% of venture partner roles are held by men, depending on what you are measuring. Social networks in venture tend to fall along gender, racial, and income lines, not because anyone is actively excluding people, but because network formation is a social process and social processes reflect the demographics of the people doing the connecting.

Research from UC Irvine and the University of California system documents this dynamic in detail: the insular nature of venture investor networks effectively quarantines capital away from outsiders regardless of the quality of their business. A warm introduction in venture capital is not just a referral. It is often evidence of prior exits, shared educational pedigree, or existing relationships with the firm’s existing portfolio. That is not a filter for quality. It is a filter for membership in a very specific social network.

The first structural change Astia made was to eliminate this requirement entirely. Any company can submit directly to Astia without an introduction. Sharon pointed out in our conversation that this is foundational: you cannot claim to be removing bias from your process while maintaining a gatekeeping mechanism that is structurally biased from its first step.

Pattern matching and its costs

Pattern matching is the cognitive shortcut where investors evaluate founders against a mental archetype of what a successful entrepreneur looks like. The archetype that has dominated Silicon Valley for decades is specific: a young, often college-dropout male, contrarian, gruff, comfortable with public confrontation, and projecting the visual and verbal markers associated with prior venture success.

Sharon is clear-eyed about what this means in practice: women and people of color do not tend to fit this pattern, not because they are less capable, but because the pattern was built from a narrow historical sample and is being applied as though it is universal.

The racial dimension of this bias is measurable. A correspondence study from Columbia University found that implicit racial bias heavily influenced which founders received high-contact interest from investors, even when credentials, including Ivy League degrees and prior successful exits, were identical. Minority founders faced more defensive, downside-focused questioning while white male founders received visionary, upside-focused questions. Same credentials, different treatment.

Astia’s response to this is to restructure the evaluation process so that pattern matching has no surface to attach to. The first two stages of the Expert Sift evaluate only written materials, with no names, no faces, no pitch dynamics, and no network signals in the room.

VC partner gender breakdown vs. portfolio gender breakdown

What the research shows about pitch bias

The venture industry has built an entire culture around the quality of the pitch. The research on this process is direct: it does not measure what it claims to measure.

A widely cited study from Harvard, MIT, and Wharton, published in the Proceedings of the National Academy of Sciences, ran controlled experiments where the content of entrepreneurial pitches was held identical while the gender and appearance of the presenter varied. Investors overwhelmingly preferred pitches from male presenters. Attractive men rated highest for perceived fundability. The evaluation was measuring presentation style and demographic presentation, not business quality.

Research on written business plans offers a different picture. Studies published in the Journal of Business Venturing found that evaluating written plans requires analytical engagement with strategy, financial modeling, and business logic, and that this format separates the structural quality of the business model from the demographic characteristics of the founder. Harvard research specifically found that investors evaluate written proposals consistently across gender when the founder’s identity is not visible.

This is the foundation of Astia’s written-word-first approach. As Sharon described it: you read the business before you meet the team. By the time you are meeting the founder, you have already formed a view of the business independent of how they present in a room.

Building a different kind of funnel

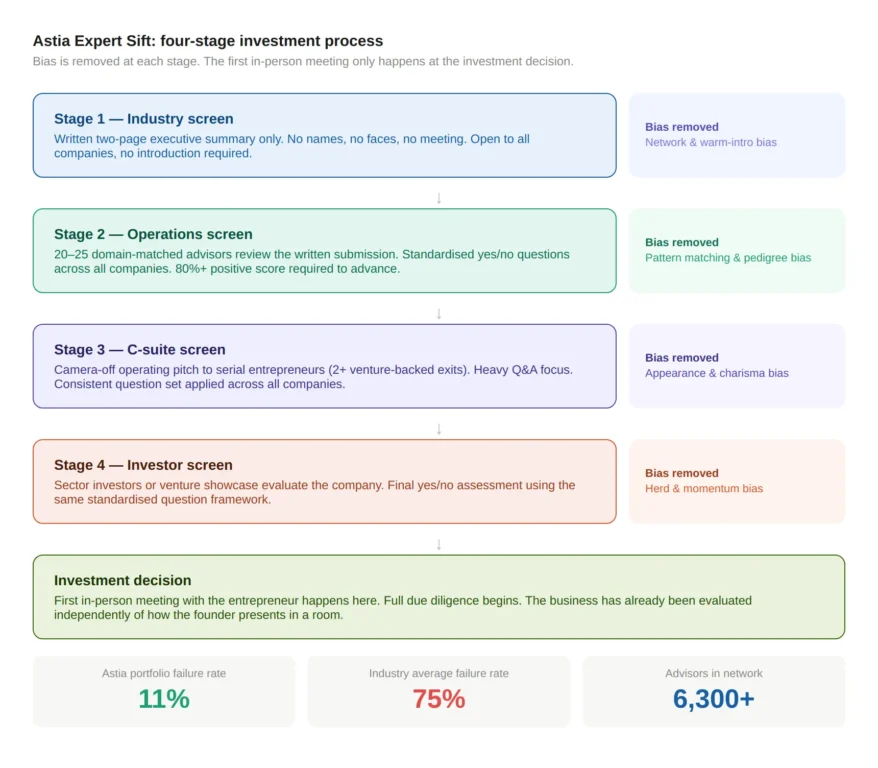

The Expert Sift operates as a four-stage process: industry screen, operations screen, C-suite screen, and investor screen. The first two stages are conducted entirely through written submission, evaluated by a network of over 6,300 advisors who are matched to companies based on domain expertise. Advisors answer a standardized set of yes/no questions that do not vary across companies. Scoring is mathematical, not impressionistic. Companies need an 80% or higher positive score to advance.

Critically, cameras are off for most of the process. The first time an Astia investor meets an entrepreneur face to face is when the firm is already considering investing. At that point, a substantial amount of objective evaluation has already taken place, and the meeting cannot retroactively introduce early-stage pattern matching.

The Expert Sift — four-stage funnel diagram

The process also benefits founders who do not make it through. Astia shares all feedback from every evaluation stage with every company, whether they advance or not. This transparency builds relationships. Companies that are too early for the fund often return when they reach the right stage, already knowing Astia and already knowing where they stand.

The industry is starting to catch up

Astia is not the only firm thinking about this. The Institutional Limited Partners Association has introduced an updated Due Diligence Questionnaire (DDQ 2.0) and Diversity Metrics Template, giving LPs a standardized framework to evaluate a fund’s approach to sourcing, screening, and DEI during the diligence process.

Other firms have moved further. Connetic Ventures uses a proprietary AI platform to automate early-stage screening with no human intervention in the initial pass. The result: 42% of their portfolio companies are led by women or minorities, investing completely sight unseen. Kapor Capital uses a structured Founder’s Commitment that evaluates founder potential through distance-traveled metrics rather than raw pedigree.

Data from Carta’s fund economics research supports the operating logic behind these approaches: smaller funds, which tend to require tighter discipline and cannot rely on momentum-based herd investing, frequently rival or outperform larger funds.

The results that make the case

Across venture capital broadly, Correlation Ventures has documented that 64% of venture-backed deals fail to return even the invested capital. That figure reflects years of gut-feel investing, network-driven deal sourcing, and pattern-matched selection. It is a very expensive tolerance for bias.

Astia’s 11% portfolio failure rate is the result of removing as many of those bias introduction points as possible. What the data shows, across more than a decade of fund activity and over 50 investments, is that a structured, documented, repeatable process produces substantially better outcomes than the industry default.

The strongest argument Sharon makes for this model is not that it is more ethical. It is that it finds better companies. By widening the aperture at the top of the funnel and removing the non-financial filters that block qualified founders, Astia reaches companies that the rest of the market has not priced correctly. That is the investment case, and it is one the performance data supports.

🎙 Listen to the full conversation with Sharon Vosmek on the SRI 360 Podcast: Episode #126

For more interviews with leading SRI, ESG, and impact investors, visit sri360.com/podcast.