Venture capital markets are supposed to be efficient. Capital is supposed to flow toward the highest-quality opportunities, and skilled investors are supposed to identify and back the best teams. That is the industry’s self-image. The data, however, tells a very different story, and for investors paying close attention, that gap between narrative and reality is where the opportunity lives.

I recently spoke with Sharon Vosmek in January 2026, CEO of Astia, one of the most data-grounded voices working at the intersection of gender-lens investing and early-stage venture capital. With 20 years at Astia and a background rooted in economics rather than the traditional venture track, Sharon has spent two decades studying exactly why capital fails to reach women-led companies, and what that failure actually costs investors.

The numbers that have not moved

Start with the most striking fact in this conversation. In 2025, venture capital investment into companies with women CEOs dropped to below 1.2% of total capital deployed in the United States. Sharon noted this figure came out just before we spoke, and it is even lower than the 2% figure often cited in prior years.

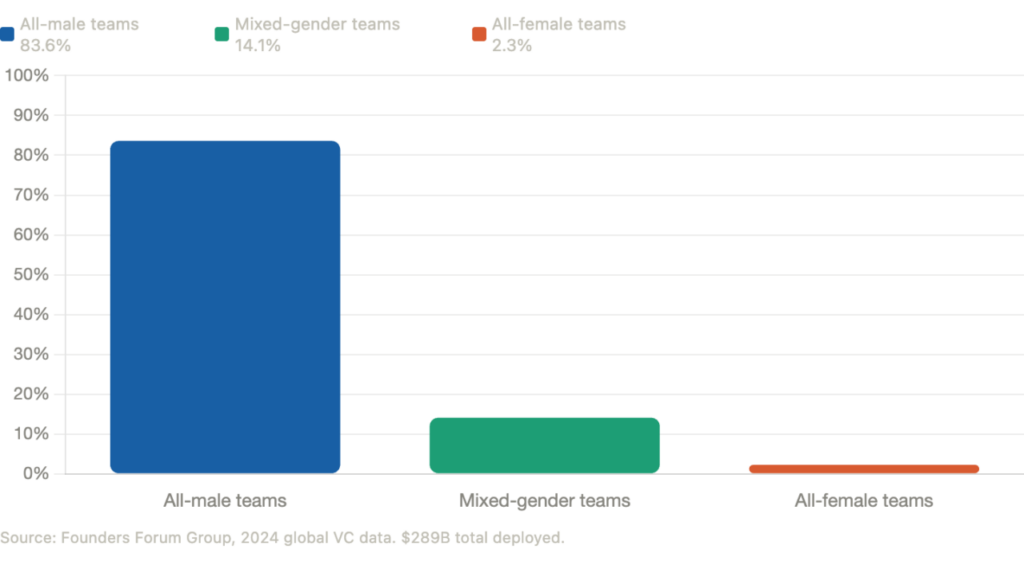

To put that in context: according to PitchBook’s Female Founders Dashboard, companies founded solely by women captured approximately 1.0% of total U.S. venture capital in 2024, down from 2.0% in 2023. Globally, according to analysis compiled by Founders Forum, female-only founding teams received just 2.3% of the $289 billion invested in venture globally in 2024.

VC funding allocation by founder gender (2024 global data)

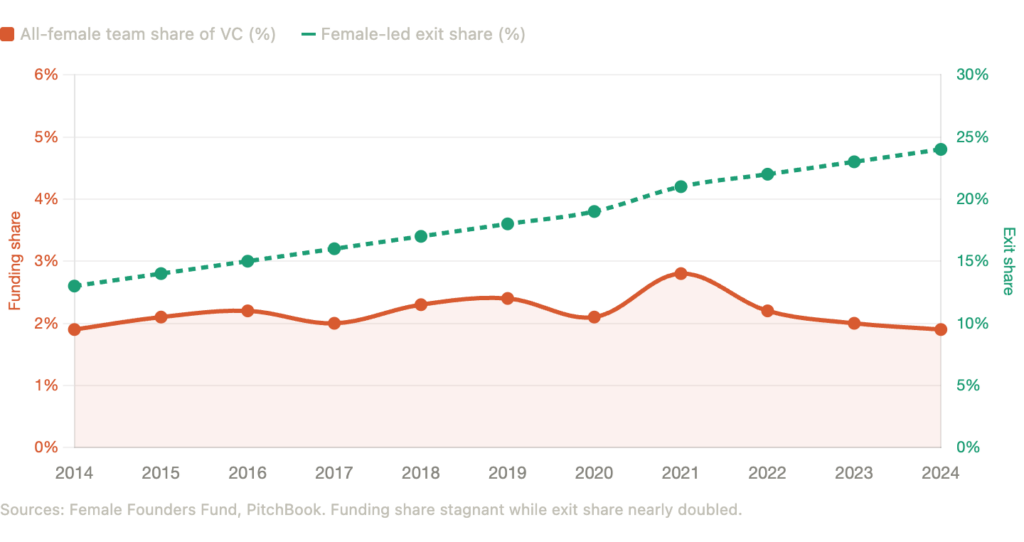

What makes this remarkable is how little the number has moved. Sharon made this clear: when she joined Astia in 2004, the figure was 1.7%. Two decades later, the needle has barely shifted. Between 2014 and 2024, the proportion of venture funding awarded to all-female teams hovered consistently between 1.9% and 2.8% globally, regardless of market cycle, according to data tracked by the Female Founders Fund.

The flat line — women-only team funding share, 2014 to 2024

Mixed-gender teams do somewhat better. They captured 14% of total capital in 2024. But Sharon is direct about what that number means in the context of a high-growth economy: it is better, but it is not right.

The pipeline myth and the human capital paradox

The standard explanation from venture general partners has long been a so-called pipeline problem: there simply are not enough highly qualified women to back at scale. Sharon dismisses this with the precision of the economist she is.

The demographic data is unambiguous. Women now earn 53% of all doctorates awarded to U.S. citizens and permanent residents, per the National Center for Science and Engineering Statistics. They represent 58.1% of all U.S. graduate students, hold 59.8% of master’s degrees, and make up close to half of first-professional degree holders including law, according to National Center for Education Statistics data.

The mathematical dissonance is stark. Women hold the majority of advanced degrees and yet receive barely 1% to 2% of venture capital. As Sharon put it in our conversation, there is simply no economic model that produces this outcome if the market is functioning efficiently. That is the heart of her argument, and it is a serious one.

The human capital paradox, degrees held vs. capital received

What the performance data shows

If the pipeline argument fails on demographic grounds, it fails even more decisively on financial grounds. The evidence that women-led companies outperform has been building for years and is now substantial.

Research from Boston Consulting Group found that female-founded companies generate 78 cents of revenue for every dollar of funding raised, compared to just 31 cents for male-founded startups. That is more than twice the capital efficiency. First Round Capital found that portfolio companies with at least one female founder outperformed all-male teams by 63%.

McKinsey research shows companies in the top quartile for gender diversity on executive teams are 21% more likely to experience above-average profitability.

BCG’s innovation research found that companies with above-average diversity on leadership teams report 19% higher innovation revenues.

Researchers at Yale School of Management, working alongside colleagues at Wharton and the University of Toronto, examined male and female co-founders of the same startups and found zero evidence that women-founded businesses provide less favorable outcomes to investors. Exit probabilities via IPO or acquisition were equal. Yet women faced substantially more friction securing follow-on capital. The researchers concluded the funding gap is not rooted in business fundamentals. It is a supply-side failure driven by investor behavior.

Sharon’s own portfolio data adds a sharper point. Astia’s portfolio carries an 11% failure rate against an industry average closer to 75%. The women’s health companies within the portfolio return on average four times the invested capital compared to the rest of the life sciences portfolio.

The exit story that changes the framing

One of the most important data points Sharon raised came from this year’s J.P. Morgan Healthcare Conference. A report published in January 2026 by AOA Dx, titled Follow the Exits: Why Women’s Health Is a Smart Bet in Healthcare, analyzed 272 publicly announced exits between 2000 and 2024 in the women’s health category. The total disclosed exit value exceeded $91 billion. Including 2025 transactions, the figure crossed $100 billion, with 27 distinct unicorn exits identified over two decades.

The reason these numbers surprised institutional investors is that women’s health companies were systematically miscategorized in databases like PitchBook and Crunchbase under broad labels such as oncology or diagnostics, making the category’s scale effectively invisible to standard sector screens.

The structural bias at the top of the funnel

Sharon’s argument does not stop at documenting the gap. She traces it to a specific structural source: the demographics of who controls the capital. As of early 2025, women hold only 15% to 17% of partner or decision-making roles at U.S. venture firms managing more than $50 million in AUM, according to data compiled by Theanna. That means roughly 83% of check-writing authority remains male-controlled. Less than 5% of venture firms have a majority of female partners.

Venture capital as an industry relies heavily on homophily, the well-documented sociological tendency of individuals to trust and associate with people similar to themselves. When that tendency governs capital allocation decisions, the demographic composition of the allocators shapes the demographic composition of the recipients. That is not a social observation. It is a structural feedback loop with measurable financial consequences.

Sharon is precise about where the problem lives. It is not in the entrepreneurs. It is in the processes and incentive structures on the investor side. Her 20 years at Astia have been spent constructing a counter-model, one that broadens the aperture at the top of the funnel in order to invest with ruthless discipline at the bottom.

The macroeconomic stakes

The opportunity cost of this market failure is significant at a macro level. Research by Babson College, in partnership with the Women Entrepreneurs Finance Initiative, estimates that closing the gender gap in business growth globally could add over $ 2 trillion to global GDP. The McKinsey Global Institute puts the broader prize of advancing women’s equality in labor and entrepreneurial markets at between $ 12 trillion and $28 trillion in global growth potential.

A landmark World Bank and IFC report on venture capital and the gender financing gap found that entrepreneurial accelerator programs actually exacerbate the funding gap rather than close it, primarily shifting female-led startups toward debt rather than equity. The researchers were explicit: the problem is not the behavior of female founders. It is the behavioral bias of the investors evaluating them.

A different framework for understanding the gap

What Sharon is building at Astia is not a social program dressed up as a venture fund. It is a structured investment thesis grounded in a specific observation: when a market systematically misprices high-quality assets due to non-financial factors, disciplined investors who correct for that mispricing capture alpha. The gender gap in venture capital is that kind of mispricing, and it has been documented, measured, and validated over 25 years of Astia’s own portfolio history.

For investors serious about return generation, the conversation Sharon is having is not about diversity for its own sake. It is about identifying and backing the most capable teams in markets that others are failing to evaluate properly. That is a different conversation, and in today’s environment, a more urgent one.

🎙 Listen to the full conversation with Sharon Vosmek on the SRI 360 Podcast: Episode #126

For more interviews with leading SRI, ESG, and impact investors, explore the full archive at sri360.com/podcast.