Most conversations about climate-smart agriculture end up at one of two extremes. Either they focus on smallholder farmers in Sub-Saharan Africa or South Asia, where development capital and microfinance are trying to build resilience from the ground up, or they focus on high-tech vertical farms and indoor growing systems, where venture capital chased the promise of hyper-efficient urban food production. Both are legitimate areas of work. Neither is where the majority of the world’s food is actually grown.

I recently spoke with Sarah Nolet, co-founder and Managing Partner of Tenacious Ventures, about what she calls the productive middle of agriculture. Her argument is that the commercial family farms sitting between subsistence smallholders and multinational agribusiness corporations control most of the world’s arable land, produce most of the world’s food, and represent the single greatest point of leverage for climate impact in the entire food system. And they are, by and large, being ignored by the investors who most loudly claim to care about agricultural sustainability.

Where the land actually is

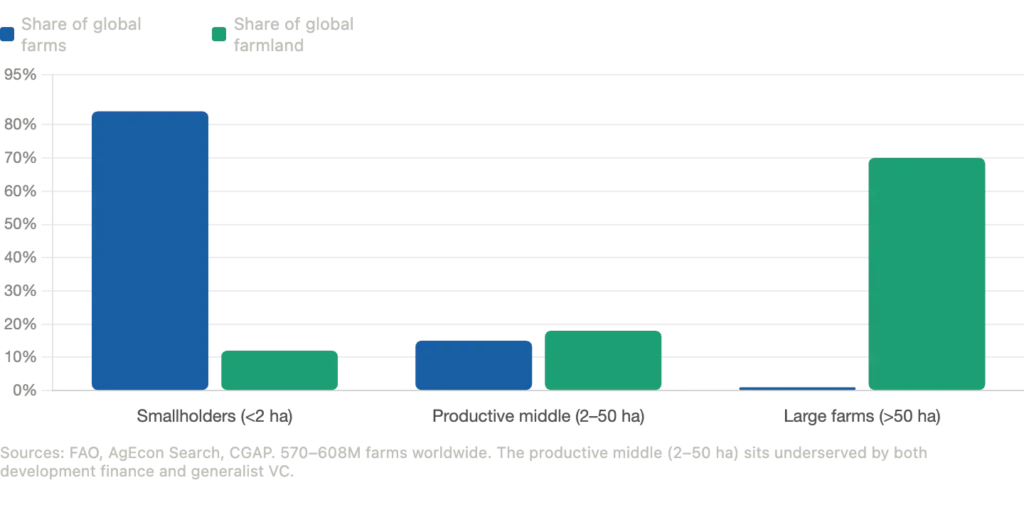

The starting point for Sarah’s argument is a simple statistical reality that tends to get lost in the narrative around smallholder farming. According to data from the Food and Agriculture Organization (FAO), there are between 570 million and 608 million individual farms worldwide. Of those, 84% are smallholder operations managing less than two hectares of land. Yet those farms, despite their enormous numbers, control only about 12% of global agricultural landmass.

The other end of the spectrum tells the opposite story. The largest 1% of farms globally, those exceeding 50 hectares, operate more than 70% of the world’s farmland. Family farms, including both small and mid-to-large scale commercial operations, manage approximately 75% of the world’s agricultural land and are responsible for producing roughly 80% of the world’s food in terms of total economic value.

Global agricultural land distribution: the productive middle paradox

What this data reveals is that the farming operations with the greatest geographic footprint and the greatest potential for scaled climate impact are not the subsistence operations that receive the most development attention, nor the corporate mega-farms that are easy targets for critics. They are the mid-to-large commercial family farms: sophisticated business owners managing hundreds or thousands of acres, making capital allocation decisions based on return on investment (ROI), operating without government subsidies in many markets, and responsive to technologies that genuinely move the needle on their bottom line.

This is what Sarah means by the productive middle. And this is where she has built the entire thesis of Tenacious Ventures.

The funding mismatch

Despite controlling the majority of the world’s farmland, this cohort of commercial operators is consistently underserved by both development finance and venture capital. According to research by the Climate Policy Initiative, annual tracked climate finance directed specifically toward small-scale agriculture sits at approximately $10 billion globally, a tiny fraction of the estimated $105 billion to $238 billion in annual investment that small-scale agriculture actually needs for climate adaptation and resilience.

Venture capital, meanwhile, has historically concentrated its agricultural investments on the same two extremes that dominate the narrative: consumer-facing software platforms, eGrocery delivery apps, and alternative protein products on one end, and development-oriented smallholder tools on the other. The commercial family farm, which requires capital-intensive hardware, agronomic expertise, and patient timelines, has largely fallen between the two.

The result, as Sarah puts it, is a $1.1 trillion annual funding gap for climate-smart agrifood systems. That figure comes from a joint report by the Climate Policy Initiative and the FAO, which found that aligning global food systems with a 1.5-degree pathway requires nearly 40 times current investment levels. The FAO is the United Nations agency that leads international efforts on food security and agriculture. Sarah is clear that the problem is not simply the quantity of money. It is whether the business models are mature enough to deploy it effectively and whether the capital is structured for the physical realities of the sector.

Why agriculture is a climate problem that cannot wait

The scale of the opportunity is matched by the scale of the problem. Global agrifood systems emitted 16.5 billion tonnes of CO2 equivalent in 2023, representing an increase of 21% since 2001 and accounting for roughly a third of total global anthropogenic greenhouse gas emissions. Nearly half of those emissions, 49%, occur within the farm gate itself, from crop and livestock activities, fertilizer application, and enteric fermentation.

The Intergovernmental Panel on Climate Change (IPCC) estimates the total technical mitigation potential from crop and livestock activities at 2.3 to 9.6 billion tonnes of CO2 equivalent per year by 2050, driven primarily by soil carbon sequestration, reduced nitrous oxide emissions through optimized fertilizer use, and improved manure management. These are practices that scale on commercial farms, not in vertical growing systems.

Precision agriculture technologies applied to commercial-scale operations have been shown to improve crop yields by 20% to 30% while cutting input waste by 40% to 60%. Smart irrigation networks deployed on commercial farms can boost water use efficiency by 40% to 60%. These are not theoretical outcomes. They are documented results in operations that already have the land base and infrastructure to adopt them.

The leverage that commercial farms offer

Why does targeting the productive middle offer more climate leverage than either extreme? Sarah’s answer is rooted in a concept she applies consistently: where do the incentives actually lie?

Commercial family farmers are not operating for ideological reasons. They are running businesses that are exposed to input costs, weather volatility, labor shortages, and commodity price swings. When a technology genuinely reduces their fuel bill, reduces their chemical spend, or allows them to do a job they cannot currently do because they cannot hire enough people, they adopt it. And when they adopt something, they adopt it at scale across hundreds or thousands of acres.

USDA data confirms this pattern. In 2023, Global Positioning System (GPS)-guided auto-steering systems were used on 70% of large-scale crop farms in the United States, and 52% of midsize commercial farms. These systems cost tens of thousands of dollars per vehicle. Farmers bought them in vast numbers because the ROI was undeniable: reduced seed and fertilizer overlap, lower operator fatigue, and better field utilization.

Sarah made a point in our conversation that challenges the conventional wisdom about farmer conservatism. Farmers are often described as slow adopters. She pushes back on this directly. Farmers are business owners managing extreme amounts of risk. They are not going to buy something that does not work for their system. But when something really works, farmers adopt it faster than almost any other sector. She cites GPS and genetically modified organism (GMO) seeds as examples of technologies that moved through commercial agriculture faster than the iPhone moved through consumer markets.

Australia as a proving ground

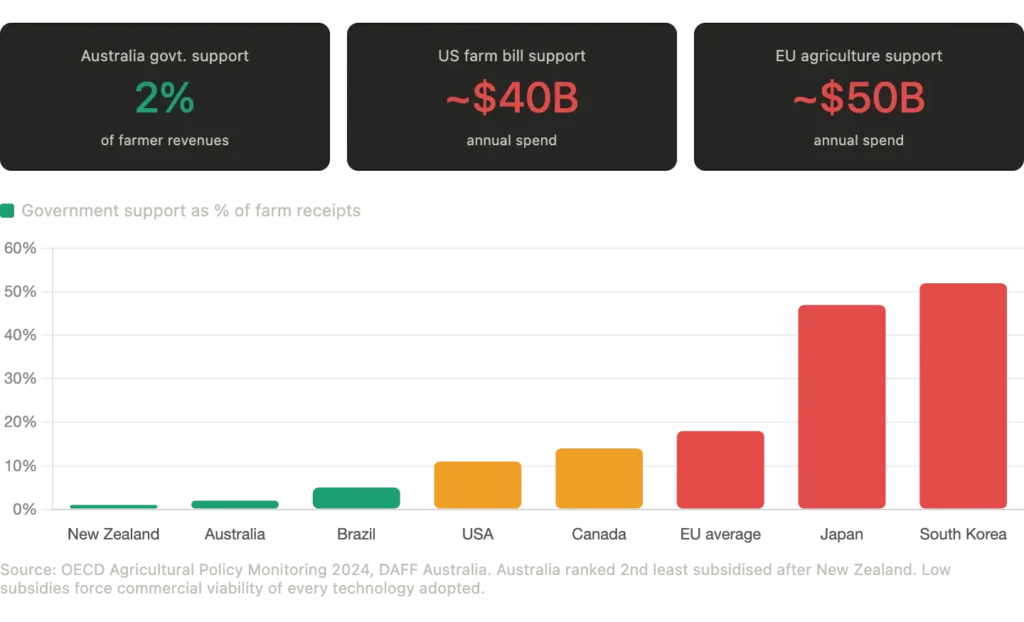

Tenacious Ventures is based in Australia, and Sarah makes a specific and compelling argument for why Australia functions as what she calls a crystal ball for global agtech adoption. The core of the argument is subsidy structure. According to data from the Organisation for Economic Co-operation and Development (OECD), Australia is the second least subsidized agricultural economy in the developed world after New Zealand. During the 2016 to 2018 period, only 2% of Australian farmer revenues came from government support, and highly distorting measures like direct price support comprised less than 1% of gross farm receipts.

This matters for technology adoption in a way that is easy to underestimate. In heavily subsidized markets, a technology does not have to deliver immediate and unambiguous ROI because farmers have a cushion. In Australia, there is no cushion. Poor soils, extreme climate volatility, severe drought cycles, and the absence of a farm bill equivalent mean that Australian commercial farmers adopt technologies that work and reject those that do not, quickly and without sentimentality.

Agricultural subsidy levels by country: why Australia is different

Practices like no-till farming, cover cropping, and controlled traffic farming have been standard in Australian commercial agriculture for years, driven by commercial necessity rather than regulatory incentive. Sarah’s argument is that what Australian farmers are doing today, often out of economic survival, is what farmers in the US and Europe are going to be incentivized to do in the coming decade through policy pressure and input cost increases. If a technology can survive and scale in the Australian agricultural environment, it is likely to travel well.

That is the investment thesis. Back companies solving real problems for commercial farmers in a demanding, unsubsidized market, generate proof of adoption and commercial traction, and then support those companies as they expand to the larger markets where the same problems are arriving on a slight delay.

The $1.1 trillion question

Sarah is careful about the framing of the funding gap. The $1.1 trillion figure is frequently cited as evidence that the agricultural climate problem is simply a capital shortage. She disagrees. The problem, she says, is not the money. It is whether the business models work well enough to deploy it at scale, and whether the capital is structured in a way that fits the physical and financial realities of agrifood systems.

This is a meaningful distinction. Pouring more generalist venture capital into agricultural software companies that ignore physical constraints, or into hardware companies that cannot survive the gap between prototype and commercial manufacturing, does not close the $1.1 trillion gap. It just creates more failures and more skepticism among the limited partner (LP) community that already views agriculture as difficult and unrewarding.

The opportunity, as Sarah frames it, is in the intersection of genuine farmer demand, proven technology, and investment structures that match the pace of biological systems. That is a narrower target than the total addressable market headline suggests. But it is also where the returns and the impact both live.

🎙️ Listen to the full conversation with Sarah Nolet on the SRI 360 Podcast: Episode

For more interviews with leading SRI, ESG, and impact investors, explore the full archive at sri360.com/podcast.