The case for investing in African smallholder agriculture as a climate adaptation strategy is, at this point, well supported by data. The returns on adaptation investment are documented. The need is quantified. The human impact is measurable. What has been missing is not evidence. It is financial architecture that makes the risk profile of this market acceptable to the institutional capital that needs to move.

I recently spoke with Tamer El-Raghy, Managing Director of the Acumen Resilient Agriculture Fund, about how blended finance structures are beginning to solve that problem.

Blended finance is a financing approach that strategically combines capital from public or philanthropic sources with private investment in a single vehicle. The public or philanthropic capital is deployed on concessional terms, meaning it accepts a lower return or higher risk than commercial capital would normally tolerate. By doing so, it adjusts the overall risk-return profile of the investment to a level that private investors can accept. In practice this often means a development institution takes a first-loss position in a fund, absorbing initial losses if the portfolio underperforms, so that commercial limited partners sit in a protected senior position. The goal is not to subsidize returns but to de-risk the investment enough that private capital will flow into markets it would otherwise avoid entirely. Tamer came to fund management from an unusual direction: materials science, then an MBA, then six years inside Cargill learning how African agricultural supply chains actually function at a macro level, then a role at Responsibility Investments managing private equity in African agriculture. By the time he joined Acumen to found ARAF in 2018, he had a clearer picture than most of exactly where the capital gaps were and why they had persisted for so long.

Why mainstream capital has avoided this space

Tamer is direct about the challenge he faced when he began raising ARAF’s first fund. He was a first-time fund manager, operating under a nonprofit parent organization that had spent its history deploying philanthropic capital, raising money for a thesis around climate resilience in African agriculture that was, at the time, not a phrase anyone in institutional investing was using. The sector was perceived as too risky, the ticket sizes too small, the exit paths too uncertain, and the political and currency risks too unpredictable.

None of these perceptions were entirely wrong. African agriculture does carry real macro risks. Governments can change import and export policies overnight. Currencies can lose 50% of their value in a short period. Tamer has seen both happen to companies in his portfolio. The question is not whether the risks are real. It is whether they are priced correctly, and whether there are structural tools that can make them manageable enough for institutional capital to participate.

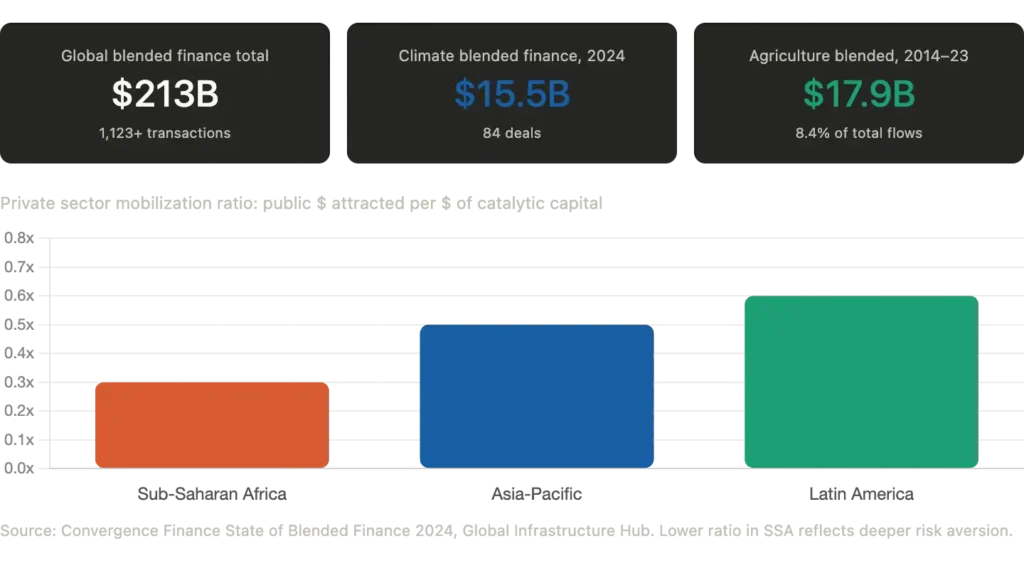

Data compiled by Convergence Finance documents the scale of the challenge. The global blended finance market encompasses over 1,123 tracked transactions representing $213 billion in total investment. Sub-Saharan Africa receives a significant share of blended finance deal flow. But the region’s private sector mobilization ratio is just 0.3, meaning that each dollar of public capital attracts only 30 cents of private capital, compared to 60 cents in Latin America and 50 cents in the Asia-Pacific. The risk aversion is real and persistent, even among investors who are already engaged in blended finance markets elsewhere.

Within the agriculture sector specifically, blended capital flows between 2014 and 2023 totaled $17.9 billion, roughly 8.4% of overall blended finance volumes. The median deal size was just $20 million, reflecting how fragmented and small-ticket agribusiness SMEs remain relative to the minimum thresholds that large institutional LPs require to deploy capital efficiently.

The mechanics of first-loss capital

The structural solution to this risk aversion is the first-loss tranche. In a first-loss structure, a catalytic investor agrees to absorb the initial financial losses of a fund up to a specified percentage. If the fund experiences defaults, weather-driven failures, or currency devaluations, the first-loss investor takes the hit first. Senior, commercial investors are protected until the first-loss buffer is exhausted.

For a fund operating in African agriculture, this changes the conversation with risk-averse LPs fundamentally. The question shifts from whether the sector is risky (it is) to whether the risk is structured in a way that the commercial investor can absorb. A 40% first-loss buffer, as the Green Climate Fund provided to ARAF’s first fund, means that the portfolio would have to lose more than 40 cents of every dollar before a commercial LP sees any impairment to their capital. That changes the risk calculus entirely.

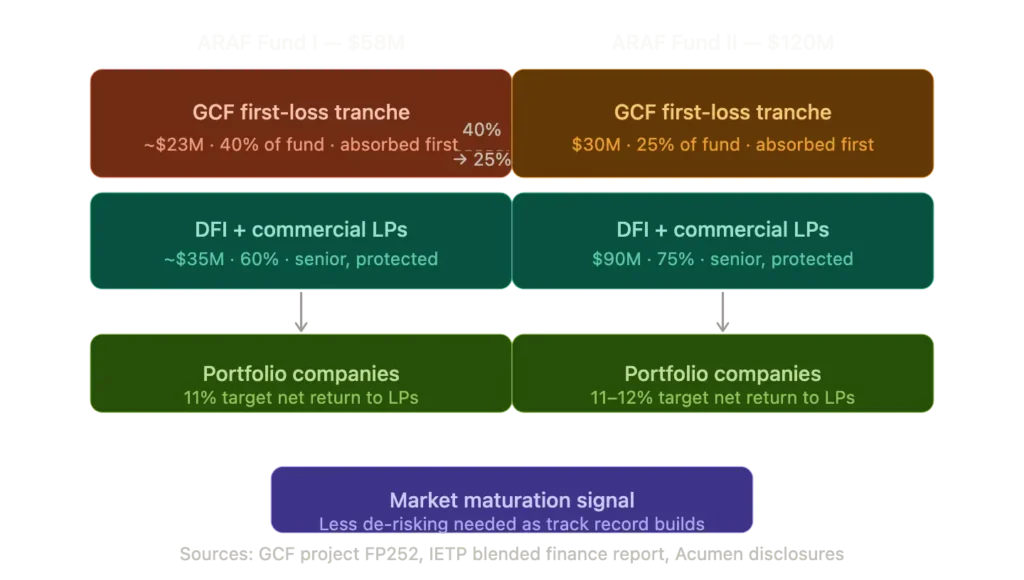

ARAF capital stack: Fund I vs Fund II first-loss structure

The Green Climate Fund has built an increasingly documented track record using this mechanism. A recent landmark example beyond ARAF is its commitment of up to $150 million in first-loss capital to anchor the GAIA Climate Loan Fund, a $1.48 billion vehicle structured with MUFG Bank and FinDev Canada to finance adaptation across climate-vulnerable markets. The principle is the same at every scale: concessional capital absorbs the risk that commercial capital cannot price, allowing private investment to flow into markets it would otherwise avoid.

ARAF as a structural blueprint

The Acumen Resilient Agriculture Fund represents the most documented application of this model in dedicated smallholder climate adaptation investing.

ARF Fund I closed at $58 million, anchored by the Green Climate Fund, which provided approximately $23 million in concessional capital representing a 40% first-loss equity position. The fund targeted net returns of 11% to 12% on the dollar, which Tamer describes as competitive within the African agribusiness space. It invested in East and West Africa, focused on companies that directly serve smallholder farmers across the physical resilience, digital infrastructure, and risk transfer themes that define the fund’s thesis.

Five years into the deployment of Fund I, the portfolio now includes companies with revenues exceeding $50 million, one company has already paid its first dividend, and the overall portfolio revenues have grown more than 3x. Every dollar ARAF invested has attracted more than $5 in co-investment from other investors. The fund has already begun returning capital to its LPs, which Tamer notes with the particular satisfaction of someone who spent years convincing skeptical institutional investors that this was possible.

ARAF Fund II is targeting $120 million, with the GCF committing $30 million, representing a 25% first-loss position matched by $90 million in co-financing from other investors. The reduction of the first-loss requirement from 40% to 25% is the most telling data point in the story. As the fund manager builds a track record, the reliance on concessional capital decreases. The market is maturing. Private investors are requiring less de-risking to participate because they can now point to five years of documented performance rather than relying on a theoretical thesis.

Tamer describes the logic plainly. When he went to raise Fund I, he was asking investors to bet on a first-time fund manager with an unproven thesis in a region many of them considered uninvestable. The first-loss structure from GCF was what made the conversation possible. Now, going into Fund II, the conversation starts differently because the proof of concept exists. The de-risking still helps at the margin, particularly for new investors seeing the fund for the first time. But the performance data is doing more of the work.

The role of DFIs and philanthropic catalysts

The GCF does not operate in isolation. The capital stack of a fund like ARAF requires participation from bilateral Development Finance Institutions and philanthropic foundations to reach commercial scale.

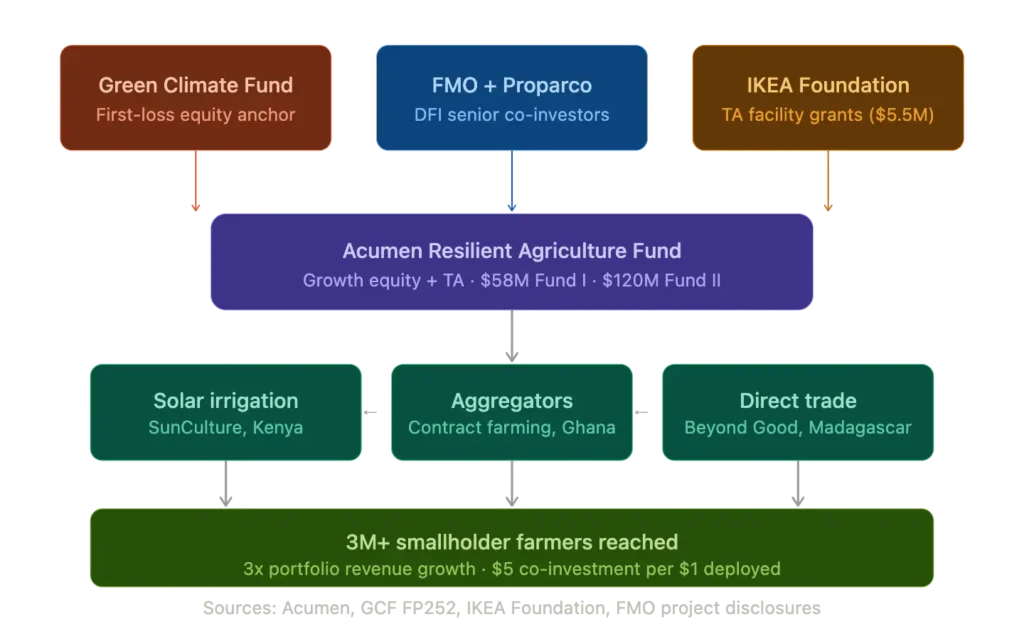

FMO, the Netherlands Development Finance Company, invested $7.5 million as an anchor in ARAF I and has committed to ARAF II. FMO’s mandate explicitly covers supporting smallholder climate resilience, and its participation alongside GCF signals to other investors that the fund has passed institutional-grade scrutiny. Proparco, the private sector financing arm of the French Development Agency, plays a similar role, providing senior capital and acting as a bridge between public donor capital and private equity in African agrifood systems.

Philanthropic capital fills a different and equally important function. The IKEA Foundation provided grant funding to establish ARAF’s $5.5 million Technical Assistance Facility, a vehicle that sits alongside the fund and provides non-investment support to portfolio companies. The IKEA Foundation also provided the grant that allowed Acumen itself to become an LP in ARAF I, an important signal of organizational commitment that helped anchor the fundraise. The Foundation’s broader strategy commits EUR 2 billion toward people-centric climate solutions, with a specific focus on linking regenerative agriculture and solar energy to build resilient food systems across East Africa.

Tamer explains the logic of the Technical Assistance Facility clearly. Earlier-stage companies in frontier markets often have things they need to do to grow but cannot afford to pay for. An ERP system, a go-to-market strategist for a new product, coaching for a middle manager ready to move into a senior role. These are not investment returns. They are capacity-building interventions that make the underlying investment more likely to succeed. The TA facility, funded entirely by grants, provides that support at no cost to the fund’s returns.

The ARAF ecosystem: who provides what

What the returns data actually shows

The narrative that impact investing requires a concessionary financial trade-off is increasingly contested by the data. Research by the Global Impact Investing Network shows that 75% of impact investors target risk-adjusted, market-rate returns. The GIIN’s State of the Market 2025 report notes a compound annual growth rate of 21% in impact AUM over the past six years.

Within the African context specifically, benchmarks tracked by market observers suggest that top-tier impact investments in African markets have yielded returns in the range of 8% to 12% over the past five years. ARAF targets the upper end of that range at 11% to 12% net to LPs, which Tamer is careful to position not as exceptional but as competitive. The point is not that this is a spectacular return by any standard. It is that it is a real return, documented, auditable, and comparable to what investors are being offered elsewhere in the impact space.

Tamer has a useful framing for the broader misperception. His fund is perceived first as an agricultural fund, and climate adaptation is what he describes as the cherry on top. The investment conversation starts with whether the companies are good businesses in viable markets. The climate adaptation thesis is the additional layer that differentiates the portfolio and justifies the impact reporting. If the companies are not financially sound, the climate case does not matter.

The regulatory friction still in the way

Despite the growing appetite for this kind of investment and the demonstrated returns, institutional LPs in Europe and the US face regulatory headwinds that make participation harder than it should be.

Under Basel III implementations in the EU and UK, commercial banks must hold substantial capital reserves against assets deemed high-risk. Blended finance vehicles in African agriculture typically lack long-term credit ratings and are domiciled in emerging markets, attracting punitive risk weightings even when first-loss guarantees are in place. If the guarantor is not an OECD sovereign or a highly rated multilateral, the commercial investor still has to hold elevated regulatory capital, which effectively prices many institutional participants out of participation.

The UK Climate Financial Risk Forum has pushed for enhanced resilience frameworks and regulatory relief, arguing that the current capital adequacy rules do not adequately recognize the de-risking impact of first-loss structures. The EU is exploring similar refinements. These are not immediate fixes, but they represent an acknowledgment that the regulatory architecture is part of what is keeping mainstream capital out of the adaptation markets that need it most.

Tamer’s view on this is pragmatic. You work with the structures that exist, not the ones you wish existed. The blended finance model works within the current regulatory environment because the first-loss layer takes enough risk off the table that even conservatively managed institutional capital can participate. Improving the regulatory environment would accelerate the flow of capital. The current environment does not prevent it.

Blended finance mobilization ratios and deal flow by region

🎙️ Listen to the full conversation with Tamer El-Raghy on the SRI 360 Podcast: Episode 127 – From Mud Huts to Brick Houses: Venture Capital & Climate Resilience in Africa

For more interviews with leading SRI, ESG, and impact investors, explore the full archive at sri360.com/podcast.