There is a phrase Sarah Nolet uses that cuts through a lot of the noise around agrifood technology investing: you cannot eat software. It is deliberately blunt, and it is meant to be. The point is not that software has no place in agriculture. It is that agriculture is fundamentally a physical system involving soil, water, biology, and machinery, and that a venture capital model built entirely around the economics of Software-as-a-Service (SaaS) businesses will consistently misread both the opportunities and the risks in this sector.

I recently spoke with Sarah Nolet, co-founder and Managing Partner of Tenacious Ventures, about what a venture capital model actually designed for agrifood systems looks like, why it requires different fund structures, different reserve strategies, and different expectations around timelines and capital intensity, and why those differences are a feature rather than a bug.

The problem with applying software thinking to physical systems

Between 2021 and 2024, the agrifood tech sector experienced one of the most dramatic boom-and-bust cycles in modern venture history. Total global funding peaked at a historically anomalous $51 billion in 2021, fueled largely by zero-interest-rate capital flooding into downstream food delivery apps, eGrocery platforms, and alternative protein brands. By 2023, total funding had fallen to $15.6 billion, a 49% decline, and some of the most heavily funded subsectors had nearly collapsed entirely.

Novel farming systems, the category that includes vertical farming, saw funding fall 79% year on year in 2023. Cloud retail infrastructure dropped 75%. Innovative food, which includes alternative proteins, fell 51%. These were not sectors that ran out of market demand. They were sectors where the investment thesis ignored fundamental physical and economic constraints. Vertical farming required enormous and ongoing energy inputs that made unit economics structurally unviable. Alternative protein brands assumed consumer behavior changes that did not materialize at the prices required to generate returns.

Sarah was watching all of this from Australia and drawing a consistent conclusion. Technology first is not the way to think about investing in the food and ag system. Things do not scale because of the technology alone. It is much more about the business model and the humans.

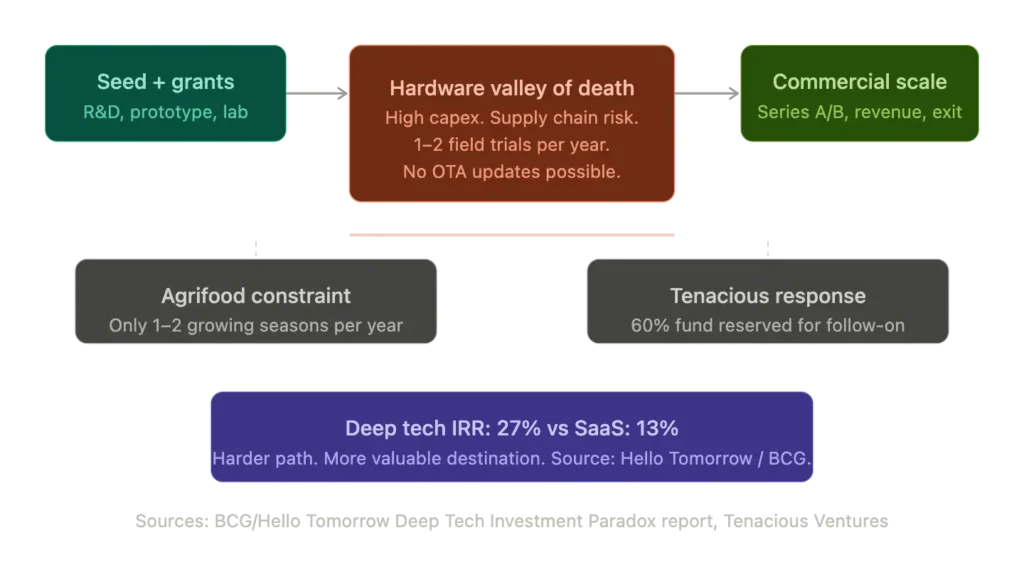

The hardware valley of death

For investors willing to look past software and engage with the physical reality of agrifood systems, the most significant structural challenge is what engineers and investors call the hardware valley of death. This is the gap between a working prototype and commercial-scale manufacturing, a chasm that kills many deep tech companies that have genuinely solved the technical problem but cannot bridge the financial gap to scale.

Analysis by Boston Consulting Group (BCG) and Hello Tomorrow found that nearly 50% of grant-funded deep tech ventures require multiple rounds of bridge funding before they can attract traditional Series A or B equity. The barriers are well-documented: high upfront capital expenditure to build prototypes, extreme process variability in early manufacturing, long regulatory pathways, and the fundamental inability to iterate rapidly the way a software company can push code.

In agriculture specifically, the biological timeline constraint makes this worse. A software company can push multiple product iterations in a day. An agricultural robotics startup testing a new autonomous field vehicle, or a biotech company trialling a novel biological crop input, has one or at most two planting seasons per year to validate results in the field. A failed trial does not just mean a delay. It means the whole calendar year is gone.

This is why Tenacious Ventures reserves 60% of its fund for follow-on capital. Most venture funds do not operate this way, and Sarah is direct about why they do. Generalist venture capital funds (VCs) frequently will not back agrifood hardware companies because they have a dollar they could otherwise put into AI. That does not mean agrifood hardware is a bad investment. It means it requires a different kind of investor who is willing to support companies through the capital-intensive stages of development that generalist funds avoid. If Tenacious’s portfolio companies need to raise that capital and there is no follow-on reserve, the fund cannot support them and risks losing the ownership position that makes the whole investment worthwhile.

The hardware valley of death in agrifood tech

When farmers adopt hardware, they move fast

The counterintuitive reality of hardware adoption in commercial agriculture is that while the sales cycle is longer and more demanding than in consumer markets, the eventual adoption rate can be extraordinary. Sarah makes this point to push back on the conventional investor view that farmers are slow adopters.

USDA Economic Research Service data confirms this at scale. In 2023, GPS-guided auto-steering systems were deployed on 70% of large-scale crop farms in the United States. These are not cheap products. They cost tens of thousands of dollars per vehicle. Farmers bought them in vast numbers because the ROI was undeniable. GPS adoption in agriculture, along with genetically modified organism (GMO) seed adoption, both moved faster through commercial farming than the iPhone moved through consumer markets once the economics were proven.

The implication for venture capital is significant. The cost of customer acquisition in agrifood hardware may be higher, reflecting the time it takes to demonstrate ROI in a real farming environment. But the lifetime value of a customer who has genuinely integrated a technology into their operation is also far higher than in most consumer markets. Farmers do not switch lightly. And once a technology has proven itself in a region, the local network effects of neighbor-to-neighbor recommendation and shared demonstration accelerate adoption rapidly.

Deep tech startups also deliver superior long-term returns when they succeed. Analysis by Hello Tomorrow found that deep tech and hardware-focused startups deliver a gross internal rate of return (IRR) of 27%, substantially outperforming software-based counterparts at 13%. The path is harder and longer. The destination is more valuable.

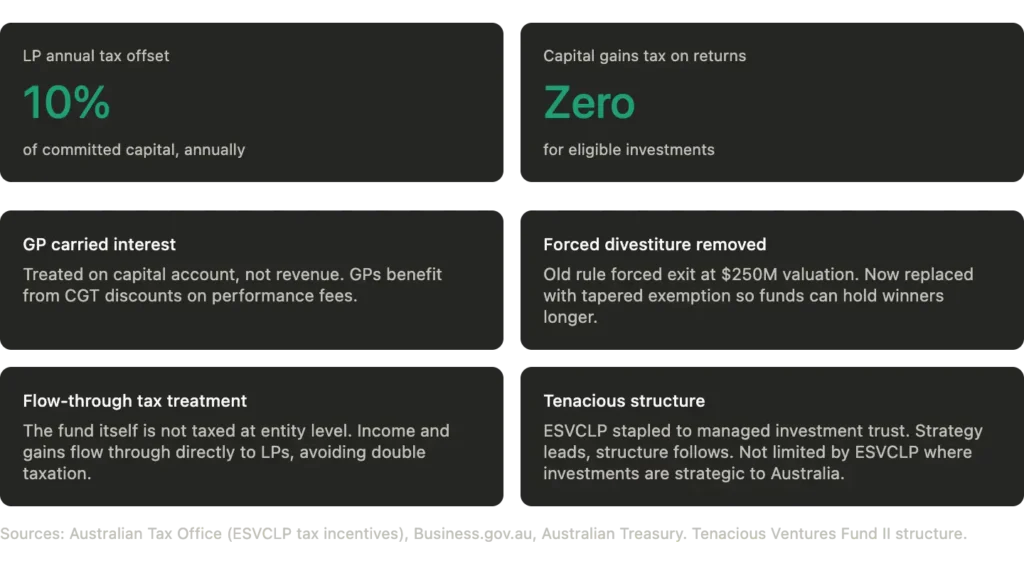

The ESVCLP structure and why it matters

One of the structural innovations that makes Tenacious Ventures’ model viable is Australia’s Early Stage Venture Capital Limited Partnership, or ESVCLP. This is a government-designed fund structure that fundamentally changes the risk-return calculus for investors backing early-stage, capital-intensive companies in sectors like agrifood hardware and biotechnology. In simple terms, the ESVCLP provides a suite of tax benefits that make it more attractive for both Australian and international investors to commit capital to early-stage Australian technology companies.

The ESVCLP provides several significant tax concessions. Limited partners receive a 10% tax offset on committed capital annually, and both Australian and foreign resident investors are completely exempt from Australian capital gains tax on returns from eligible investments. General partners can treat their carried interest on the capital account rather than as standard revenue, accessing capital gains tax (CGT) discounts. An earlier rule that forced funds to divest once a portfolio company exceeded $250 million in value has been removed, replaced with a tapered partial exemption that allows funds to hold winning companies longer.

For an investor backing deep tech agriculture companies that may take seven to nine years to reach exit, these concessions change the economics materially. The 10% annual offset on committed capital effectively reduces the cost basis of participation in the fund, and the full capital gains exemption means that when a company like SwarmFarm Robotics eventually exits to a strategic acquirer like John Deere or CNH, the return flowing to limited partners is not further eroded by tax.

Sarah is explicit about this in how she structures the fund. The strategy is strategic to Australia. The ESVCLP is the structure that enables the strategy, not the other way around. The fund is structured to take full advantage of the Australian tax benefits when investments comply with the scheme, but is not limited to companies that can only operate in Australia.

ESVCLP tax benefits: how Australia’s structure de-risks deep tech investment

Three portfolio companies that make this real

The investment thesis becomes concrete in the portfolio. Three companies from Tenacious Ventures illustrate how the atoms-not-bits framework translates into actual capital allocation decisions.

SwarmFarm Robotics, founded by Andrew and Josie Bate on their farm in regional Queensland, builds autonomous vehicles for broadacre agriculture. The business model Sarah describes is analogous to the iPhone and app store: SwarmFarm builds the robotic platform and the software that manages movement, obstacle detection, and field planning, while implement providers build the attachments that do the actual field work, whether that is spraying, mowing, or fertilizer spreading. Tenacious first invested in 2020 and has followed on in two subsequent rounds. SwarmFarm recently closed a $30 million Series B. The climate case is concrete: smaller equipment means less soil compaction, more water retention, and precision herbicide application that dramatically reduces total chemical load. The commercial case is equally concrete: it is a robot that works 24 hours a day, seven days a week, and never calls in sick, solving a severe agricultural labor shortage problem that is only getting worse.

Gotera, the fund’s first investment out of Fund I, uses modular technology with a biological process to manage organic food waste. The biological process is black soldier fly larvae, which consume organic waste and produce two monetizable outputs: a protein product for livestock feed and a fertilizer. Gotera gets paid for waste management, which is an existing commercial paradigm, and then generates additional revenue from the protein and fertilizer offtake. The impact measurement is straightforward: every tonne of organic waste processed is a tonne that does not go to landfill, with a direct and calculable reduction in landfill methane emissions. More revenue equals less methane. Sarah notes this is one of the cleanest impact-to-revenue correlations in the portfolio.

Enrio, a livestock genetic improvement company, offers what Sarah describes as IVF for cows. In vitro fertilization already exists in the livestock industry but is accessible only to the top tier of commercial producers because of cost and labor requirements. Enrio has developed both biotech for more efficient embryo creation and a medical device to simplify the implantation process. The tagline is seven years in seven days, referring to how much faster genetic improvement can be accelerated compared to conventional breeding cycles. The climate relevance is in the sustainability traits that can be introduced into commercial herds: feed efficiency, methane reduction, and heat tolerance, all of which become more commercially important as climate volatility increases.

The reserve strategy and why 60% matters

The 60% reserve strategy is not a conservative instinct. It is a deliberate response to a specific structural reality of hardware-intensive agrifood investing. Generalist VC funds have a dollar and they can put it into AI. They frequently will not back the second or third round of a farm robotics company or an agricultural biotech business because the return timeline does not fit their model and the deal sizes are too small.

If Tenacious is the right investor for these companies at the seed or Series A stage, it needs to remain the right investor at the Series B and beyond. That requires capital in reserve. It also requires a willingness to write bigger checks as the conviction builds, which Sarah frames as the most honest form of value-add: when you believe in a company, you write a check. Everything else is supplementary.

This is also where the partnership framing in Tenacious’s OCP investment framework matters most. OCP stands for Opportunity, Company, Partnership. The P is about the alignment between the fund and the founder around how much capital will be needed, what the exit target looks like, and whether a $200 to $500 million strategic acquisition by an incumbent agribusiness is a win worth building toward, rather than holding out for a unicorn valuation that the sector’s economics may never support.

Sarah’s position is clear on this. The sector does not need to mimic the standard venture model to deliver venture-grade returns. It needs a model that fits what the sector actually is.

Agrifood tech funding collapse 2021–2024 and the upstream shift

🎙️ Listen to the full conversation with Sarah Nolet on the SRI 360 Podcast: Episode

For more interviews with leading SRI, ESG, and impact investors, explore the full archive at sri360.com/podcast.