Climate finance conversations almost always begin with the same headline number. Global climate flows have now crossed $2 trillion annually, an all-time high. The system is mobilizing at scale. The problem is what it is mobilizing toward.

Before unpacking that problem, it helps to define the two categories at its heart. Mitigation finance funds efforts to reduce or prevent greenhouse gas emissions. Think solar farms, wind power, electric vehicles, and building retrofits. The goal is to slow the rate of future warming. Adaptation finance funds efforts to help communities and economies cope with climate change that is already happening or locked in. Think drought-resistant crops, flood-resilient farming systems, and insurance products that protect smallholder farmers when harvests fail. Mitigation addresses tomorrow’s problem. Adaptation addresses today’s reality for the people already living with climate consequences.

I recently spoke with Tamer El-Raghy, Managing Director of the Acumen Resilient Agriculture Fund, about a structural question that sits underneath all of these record-breaking figures. Africa contributes less than 5% of global greenhouse gas emissions, yet its farmers are absorbing some of the most severe consequences of a warming planet. The capital flowing toward that problem is, by any honest measure, a rounding error in the global climate finance system. Tamer has spent the better part of a decade building the investment infrastructure to change that. The conversation sharpened something that the data had already been telling anyone willing to look.

The $2 trillion blind spot

The headline figures in global climate finance are real. The composition of those figures is where the problem lives.

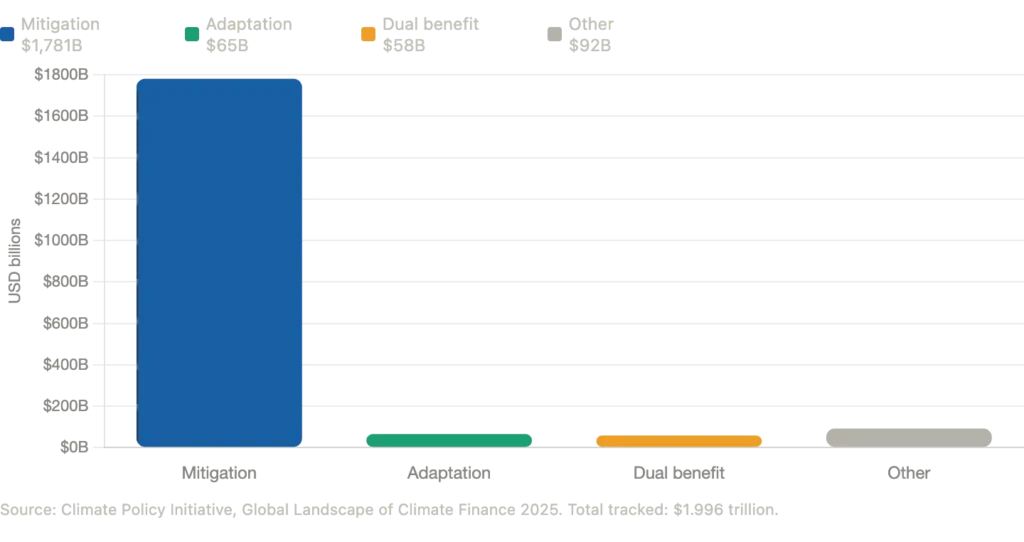

According to the Climate Policy Initiative’s Global Landscape of Climate Finance 2025, of the $1.9 trillion tracked in 2023, mitigation efforts captured $1,781 billion. Adaptation finance, the capital directed at helping communities survive and function in a warming world, received $65 billion. That is roughly 3.3% of the total. When dual-benefit projects are included, the adaptation-related share reaches approximately 5%. The rest of the capital stack is going toward renewable energy systems, electric vehicles, and building efficiency upgrades in economies that already have the infrastructure to absorb those investments.

Global climate finance split: mitigation vs adaptation

This 5% figure is not a data anomaly. It reflects something structural about how climate finance works. Mitigation projects, particularly utility-scale solar and wind, generate predictable long-term cash flows backed by power purchase agreements. They are financeable through standard commercial bank lending and institutional debt markets. Adaptation projects, by contrast, often produce what economists call avoided losses. The value they generate is a crop failure that did not happen, a family that did not fall below the poverty line, a community that absorbed a climate shock without collapsing. That value is real, but it is not easily monetized, and private capital has not figured out how to price it.

The result is a widening gap between what is needed and what is flowing. The UNEP Adaptation Gap Report 2025 estimates that developing countries will need between $310 billion and $365 billion annually for adaptation by 2035. International public adaptation finance to developing countries actually declined from $28 billion in 2022 to $26 billion in 2023. That is a 12-to-14-fold gap between need and delivery, and it is growing.

Where the money is not going

Even within the constrained pool of adaptation finance, the distribution is skewed toward hard infrastructure. Seawalls, flood barriers, and upgraded transport networks capture a disproportionate share of adaptation budgets. A Center for Global Development analysis of World Bank adaptation finance found that agriculture receives a surprisingly small portion despite accounting for roughly a quarter of GDP in the most vulnerable nations.

This matters because the communities that need adaptation finance most are not primarily threatened by coastal flooding. They are threatened by erratic rainfall, rising temperatures, and the collapse of the agricultural systems that constitute their entire economic livelihood. Redirecting adaptation capital toward hard coastal infrastructure while smallholder farmers in the interior of Sub-Saharan Africa watch their yields deteriorate is a misallocation with humanitarian consequences.

Tamer is precise about this in our conversation. The businesses he invests in are not building seawalls. They are selling solar-powered irrigation systems on payment plans, connecting farmers to guaranteed off-take markets, and distributing dual-purpose poultry that give families a stable income stream between harvests. These are adaptation investments in the most literal sense, and they are almost entirely absent from the tracked flows of global climate finance.

The injustice gap

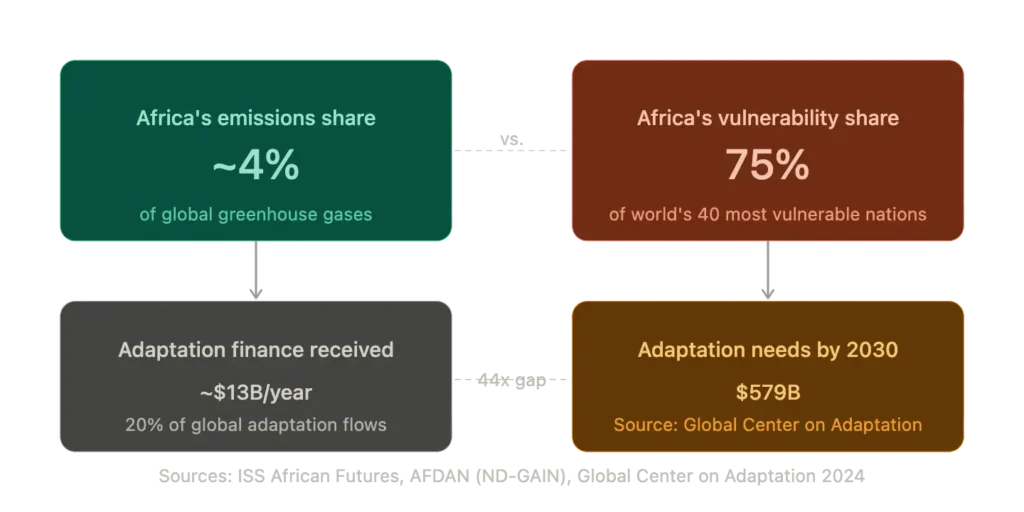

The moral dimension of this misallocation is stark. The African continent contributes less than 4% to 5% of global greenhouse gas emissions. Sub-Saharan Africa alone contributes just 1.9%, and if South Africa is excluded, the remaining 48 nations account for approximately 0.6% of global emissions. On a per capita basis, the average African emits roughly one tonne of CO2 annually, compared to 10.3 tonnes in North America.

Africa’s emissions vs. climate vulnerability: the injustice gap

Despite this negligible contribution to atmospheric carbon, Africa is consistently ranked as the most climate-vulnerable continent on Earth. The ND-GAIN index places 30 of the world’s 40 most climate-vulnerable countries in Africa. In 2022 alone, more than 110 million people on the continent were directly affected by weather, climate, and water-related hazards, resulting in over $8.5 billion in economic damages.

Africa receives approximately $13 billion annually in adaptation finance flows. Its estimated adaptation needs by 2030 are $579 billion, according to the Global Center on Adaptation. The communities least responsible for the problem are absorbing the greatest share of its costs, with the least financial support to do so.

Tamer does not frame this as a purely moral argument, which is part of what makes his thesis compelling. He frames it as a market inefficiency. The communities most exposed to climate risk are also the most economically dependent on agriculture. Helping them adapt is not charity. It is the only viable path to maintaining functional food systems and economic activity in a region that will house 60% of the world’s chronically undernourished population by 2030.

What climate change is already doing to African farms

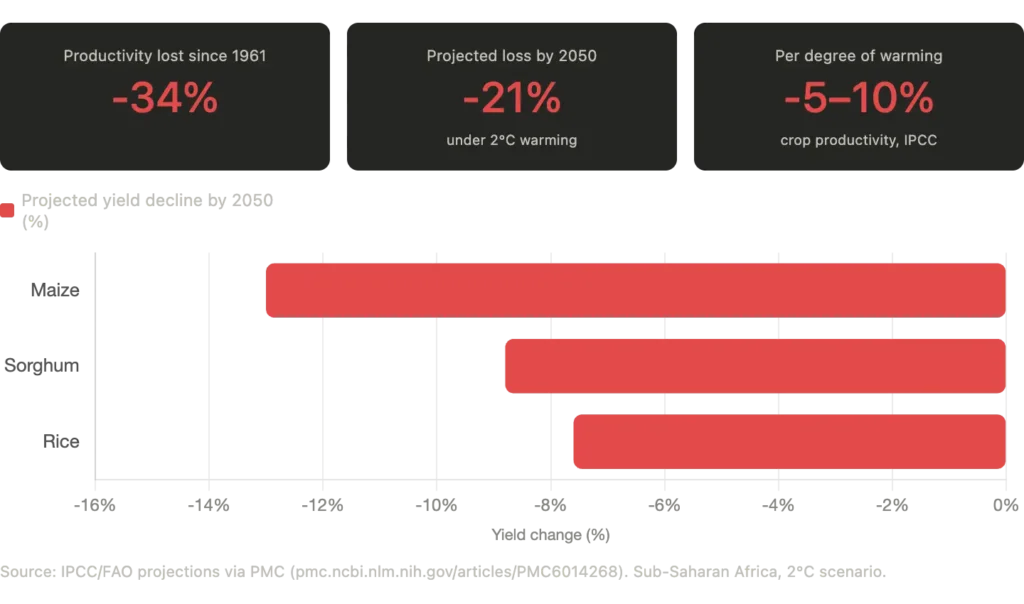

The data on existing agricultural impact is sobering. Since 1961, climate change has already decreased Africa’s total agricultural productivity by 34%. African agriculture is predominantly rain-fed, with less than 4% to 6% of agricultural land currently irrigated, making the entire system structurally dependent on precipitation patterns that are becoming increasingly unreliable.

The projections for 2050 are severe. With a 2°C temperature rise, agricultural productivity in Sub-Saharan Africa could decline by up to 21%. Maize yields are projected to fall by 13%, sorghum by 8.8%, and rice by 7.6% under the same scenario. The IPCC projects a 5-10% decline in crop productivity for every degree of warming above historical levels.

Projected crop yield declines in Sub-Saharan Africa by 2050

There are approximately 33 million smallholder farmers in Africa. In Sub-Saharan Africa, smallholder agriculture employs up to 65% of the labor force and supports the livelihoods of 60% of the population. These farmers produce over 70% of the food consumed in many specific nations. The sector is not a marginal economic activity. It is the foundation of food security and economic stability across the continent, and it is being systematically degraded by a climate crisis these communities did almost nothing to create.

The economic case for adaptation

The strongest argument for redirecting climate capital toward adaptation is not moral. It is financial. A comprehensive study by the World Resources Institute evaluating 320 adaptation investments across 12 countries found that every $1 invested generates more than $10 in benefits over a ten-year period, with an average return rate of 27%. The Global Center on Adaptation confirms benefit-cost ratios ranging from 2:1 up to 10:1 across adaptation investment categories.

The International Food Policy Research Institute estimates that a $16 billion annual investment in agriculture could prevent 78 million people from starving by 2050. That is not a social return. It is a stabilization of the food systems that global commodity markets, including the supply chains of every major consumer goods company on the planet, depend upon.

Tamer’s point in our conversation is simple and hard to argue with. The data is out there. The returns are documented. The investment case is real. What is missing is not evidence. It is the right financial structures to connect that evidence to the capital sitting in institutional portfolios.

What major institutions are saying

The major institutions are beginning to respond. At the 2024 Annual Meetings, World Bank Group President Ajay Bangacommitted to allocating 45% of total World Bank financing to climate initiatives, with a call to direct half of that toward adaptation. The Bank has also pledged to double agri-finance commitments to $9 billion annually to help smallholder farmers integrate into commercial value chains.

The Green Climate Fund, the world’s largest dedicated climate fund, operates under an explicit mandate to maintain a 50/50 balance between mitigation and adaptation in grant-equivalent terms, and to direct at least half of its adaptation resources to the most climate-vulnerable nations. By end of 2024, the GCF had allocated $15.9 billion cumulatively, and in 2025 it channeled a record $3.26 billion in new climate finance.

At the policy level, negotiations at COP29 and COP30 produced the Baku to Belém Roadmap, which sets a global target to triple adaptation finance to $120 billion annually by 2035, up from the previous $40 billion target.

These are significant commitments. But as Tamer points out, commitments from institutions are not the same as capital deployed to farmers. The gap between pledges and disbursements in climate finance is well documented. Closing it requires not just more money but better financial structures that can actually route capital to the places where it is needed. That is what the blended finance model, and funds like ARAF, are designed to do.

🎙️ Listen to the full conversation with Tamer El-Raghy on the SRI 360 Podcast: Episode — De-Risking Climate VC

For more interviews with leading SRI, ESG, and impact investors, explore the full archive at sri360.com/podcast.