Global climate finance hit a record $1.9 trillion in 2023. Early indicators suggest it surpassed $2 trillion in 2024. By almost any measure, capital is flowing into climate solutions at an unprecedented rate. And yet, a growing number of investors and climate practitioners argue that the vast majority of this money is going to the wrong place.

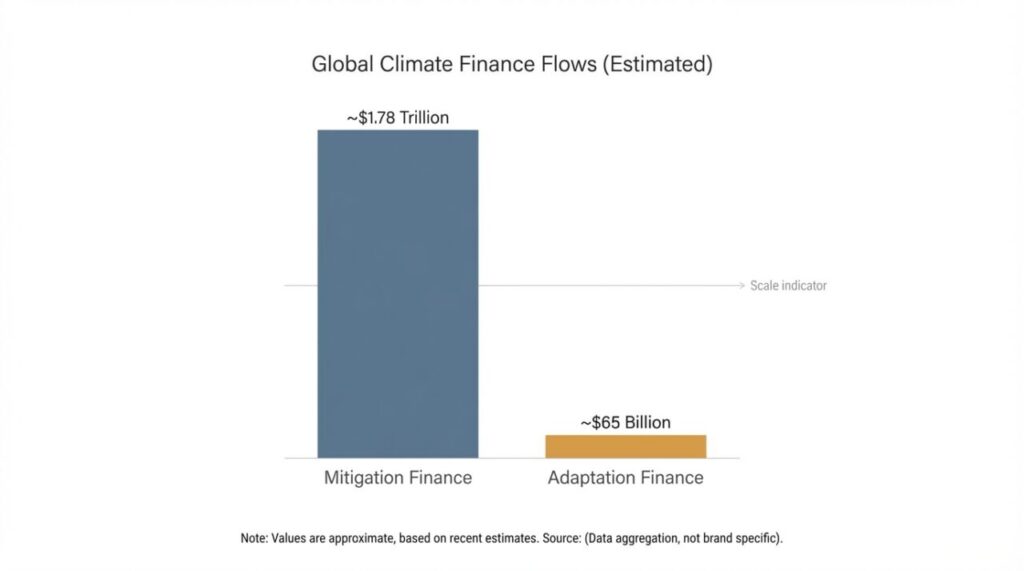

The problem is not a lack of climate capital. The problem is where it goes. Of that $1.9 trillion, approximately $ 1.78 trillion went to mitigation, meaning projects that reduce greenhouse gas emissions like solar farms, wind turbines, electric vehicles, and energy efficiency improvements. Only $ 65 billion went to adaptation, meaning projects that help communities and economies survive the climate impacts that are already happening. That is roughly 3.4% of the total.

For investors who believe they are funding the fight against climate change, this ratio deserves scrutiny. Because in the regions of the world where climate change is not a future projection but a present emergency, the money is simply not showing up.

A flooding scene in a Southeast Asian city and agricultural area, pictures the immediate reality of climate impacts in the region.

The $1.9 Trillion Misallocation Problem

I recently spoke with Alina Truhina, co-founder of Utopia Capital Management and managing partner of the Radical Fund, a Southeast Asia-focused climate tech venture capital fund. Truhina has spent more than a decade working across emerging markets, from the World Bank’s disaster recovery division to building venture platforms in Africa, and she has watched the climate finance gap widen in real time.

Her diagnosis of the problem is direct: “Mitigation is much, much easier to quantify. Whether you’re an investor or a development finance institution or a government, measuring carbon is a quantifiable measure and you can price it, you can model it, you can put it into a spreadsheet. Adaptation is harder to measure.”

This measurability gap has created a self-reinforcing cycle. Because mitigation outcomes (tons of CO2 avoided, kilowatt-hours of clean energy generated) are easier to model and report, they attract more capital. Because adaptation outcomes (losses averted, households made resilient, hectares under climate-smart practices) involve probability, assumptions, and non-linear metrics, they struggle to compete for the same institutional dollars.

The result is a global climate finance architecture that is remarkably good at funding the energy transition in developed economies and remarkably poor at protecting the people who are already being hit hardest by climate change.

According to the UNEP Adaptation Gap Report 2025, developing countries will need between $310 billion and $365 billion annually by 2035 to manage climate impacts. International public adaptation finance actually fell to $26 billion in 2023, down from $28 billion the year before. The gap between what is needed and what is flowing is now 12 to 14 times greater than current levels.

And the private sector, which accounts for over half of total climate finance globally, contributes less than 1% of adaptation finance in regions like Asia-Pacific. The money is there. It is just going somewhere else.

Data visualization showing the stark contrast between mitigation and adaptation finance flows.

Southeast Asia Is Already Living the Climate Crisis

For investors who have never spent time in the region, Southeast Asia’s climate vulnerability can feel abstract. For anyone who has, it is visceral.

Truhina describes her arrival in Bangkok with a story that captures the disconnect: “When I first landed in Bangkok, I remember people wearing masks outside, and this was just after the COVID era. Why are people wearing masks outside? Don’t they know COVID is going down? Only to then realize as my lungs filled up with polluted air that they were wearing it because of pollution. I literally couldn’t breathe.”

Annual average PM2.5 levels in Thailand reached 19.8 µg/m³ in 2024, nearly four times the WHO guideline of 5 µg/m³. But air pollution is only one dimension of the crisis. Three out of ten ASEAN countries, Myanmar (ranked 2nd), the Philippines (4th), and Thailand (9th), rank among the 10 most climate-affected countries globally.

The threats are not hypothetical. Sea levels are rising. Flooding frequency has increased significantly over the past 30 years. Heat waves are intensifying.

Monsoon patterns are disrupting agricultural cycles. Over 200,000 casualties have been recorded in Southeast Asia due to climate-related disasters over the past three decades, with storms as the primary cause of death and displacement.

And the economic stakes are enormous. Southeast Asian countries risk losing between 18% and 25% of their GDP due to climate change, with water-intensive agricultural sectors particularly at risk. The Asian Development Bank estimates the region needs $210 billion annually for climate-resilient infrastructure through 2030.

Yet the region’s GDP growth continues to outpace the global average, projected at 4.5% to 4.7% in 2024-2025 compared to the global average of 3.2%. This creates what researchers call the “resilience paradox”: the region is simultaneously one of the fastest-growing economic zones on the planet and one of the most fragile.

“It is here. It’s not going to happen in 10 years’ time or 20 years’ time,” Truhina says. “We are already being impacted.”

Why Adaptation Is Harder to Fund but Easier to Justify

The structural reasons why adaptation remains underfunded go beyond measurability. Truhina identifies a “missing middle” in the capital stack that leaves the most innovative adaptation solutions without funding.

“There’s this missing middle whereby you’ve got startups that are creating new solutions for people, for society, in the adaptation space,” she explains. “They’re too commercial for your philanthropic, concessionary, pure impact-related investors. So they might miss out on some of these large grants going toward infrastructure projects or renewable projects. But they’re too complex or too asset-heavy for VC.”

This is a critical insight. Adaptation finance has historically flowed through large government-supported funds and development finance institutions into infrastructure: seawalls, flood barriers, irrigation systems. These are necessary investments, but they are not startup investments. The startups building early warning systems, climate-resilient supply chains, parametric insurance products, and precision agriculture tools fall into a gap between grant funding and traditional venture capital.

The irony is that the economic case for adaptation investment is exceptionally strong. According to UNEP research, every $1 spent on coastal protection avoids

$14 in damages. Urban nature-based solutions can reduce ambient temperatures by over 1°C, significantly cutting heat-related productivity losses. The return on investment for adaptation is not theoretical. It is documented.

But the metrics are different. “Identifying KPIs around resilience or around risk reduction or around avoiding losses, there’s a lot of probability, a lot of hypothetical, a lot of assumptions, and a lot of non-linear, non-quantifiable metrics,” Truhina acknowledges. “So it’s harder to measure and to manage.”

This difficulty is real, but it is not insurmountable. The Radical Fund has developed what Truhina calls a “performance management framework” that integrates commercial growth metrics alongside climate mitigation and adaptation metrics.

The fund measures IRR and MOIC alongside greenhouse gas emissions avoided, households improved, and hectares of land under climate-resilient practices.

“We’re measuring your IRR and your MOIC as a fund as well as your unit economics whilst also measuring GHG emissions avoided or households improved and hectares of land under climate-resilient practices,” she explains. “It wasn’t as easy as it sounds, but we’ve integrated the two.”

A Southeast Asian farmer implementing solar-powered irrigation.

Investing Where the Capital Isn‘t

The Radical Fund launched with a first close in July 2023, targeting $40 million for pre-seed to Series A climate investments across Southeast Asia. What distinguishes the fund from other climate vehicles in the region is its deliberate focus on adaptation alongside mitigation.

“When we first had this concept of what would it take to launch a fund in Southeast Asia with a climate focus, we very quickly realized there are not many climate funds in Southeast Asia,” Truhina says. “And of those that existed, the majority, if not all of them, focused on climate mitigation. And it’s very unfortunate also that a lot of them invested outside of the region.”

This last point is particularly striking. Climate funds nominally focused on Southeast Asia were deploying capital into the US and Europe, where investments were perceived as lower risk. Approximately 30 climate-focused funds have launched in Southeast Asia since 2020, committing $830 million in total capital.

But the region received just 7% of global climate tech investment in 2024, compared to $24 billion flowing to the US alone.

Truhina’s fund deliberately inverts this pattern. The Radical Fund does not invest outside the region. Founders must be operational in Southeast Asia or have significant customer bases there. And the portfolio construction intentionally tilts toward adaptation.

“If you had to estimate what percent is mitigation versus adaptation of capital deployed from our fund, I would say roughly 60/40,” she says. In a global landscape where adaptation receives less than 4% of climate finance, a 40% allocation represents a radical departure from the norm.

The fund targets commercial returns that are indistinguishable from any other VC fund: a 3x return with above 25% IRR. Truhina is emphatic that this is not concessionary capital.

“We’re not concessionary. We’re not patient in many ways. Catalytic, yes, but we’re definitely looking for a 3x return with above 25% IRR with above 1.5 DPI.”

The thesis is that adaptation is not a charity play. It is a market opportunity created by the systematic failure of global capital to flow to where physical climate risk is highest. As temperatures rise, monsoons shift, and infrastructure degrades, the companies that help economies and communities survive will not lack for customers. The question is whether investors will recognize this before or after the market prices it in.

The Political Advantage of Emerging Markets

There is one more dimension to the adaptation investment thesis that Truhina raises, and it echoes a point made increasingly by emerging market investors across the SRI 360 podcast. In many of the regions most affected by climate change, there is no political debate about whether climate change is real.

“Southeast Asia as a region is one of the most vulnerable regions in the world due to climate change, and at the same time it’s also one of the largest emitters,” she observes. ASEAN’s share of global GHG emissions rose from 4.7% to 5.7% over the last decade, with growth of 31.3%, higher than China’s 21.3% during the same period. But unlike some developed economies, the response in the region is not paralyzed by political polarization.

For climate investors with a 70% allocation to the United States, a country where climate policy shifts with every election cycle, the stability of climate commitment

in Southeast Asia represents something valuable: policy predictability. Companies building adaptation and mitigation solutions in the region are not at risk of having their market erased by a change in government.

The global climate adaptation technology market reached $25.5 billion in 2025, with Asia-Pacific emerging as the largest regional market. The opportunity is not small. It is not niche. And it is growing faster than the capital flowing toward it.

For investors still directing 90% of their climate allocation to mitigation in developed markets, the question Truhina poses is simple: “We can see the flooding. We can see the impact on food and water scarcity. How do we bring solutions that help us adapt to this reality?”

The capital will eventually flow to adaptation. The returns will accrue to those who got there first.

To hear Alina Truhina’s full argument for climate adaptation investing in Southeast Asia, listen to the complete interview on the SRI 360 Podcast, Episode 124.

This article is based on a discussion of climate investing from the SRI 360 Podcast. For more perspectives on sustainable and responsible investing, visit sri360.com/podcast.