At an asset manager, most days are spent inside abstractions. Yield curves. Position sizes. Political transition. Central bank scenarios. It’s stimulating, often fun, and it feels serious.

Then the noise stops and you’re sitting across from a client.

In that moment, abstraction melts away and you’re simply selling trust. The question is brutally simple: why should this client trust you with their money rather than someone else?

That question is what pulled me deeper into ESG work. For clients who care about sustainability as well as returns, the industry’s narrative had become impossible to defend. We promised too much and delivered too little that was measurable, honest, or even consistent.

I am a terrible liar. And I could not keep pretending that markets already allocate capital in a way that neatly fixes climate change, inequality, or nature loss.

This article is not about killing ESG. It’s about diagnosing why it stopped making sense and why clients can feel that something is wrong even when the slide decks look polished.

Part 2 will argue that we can do better. Part 1 is the uncomfortable diagnosis.

How We Got Here

These tensions didn’t arise in a vacuum and it was not just a feel-good overlay. ESG emerged to compensate for the failure of fiscal and monetary policy to deal with environmental stress, inequality, and long-term economic resilience.

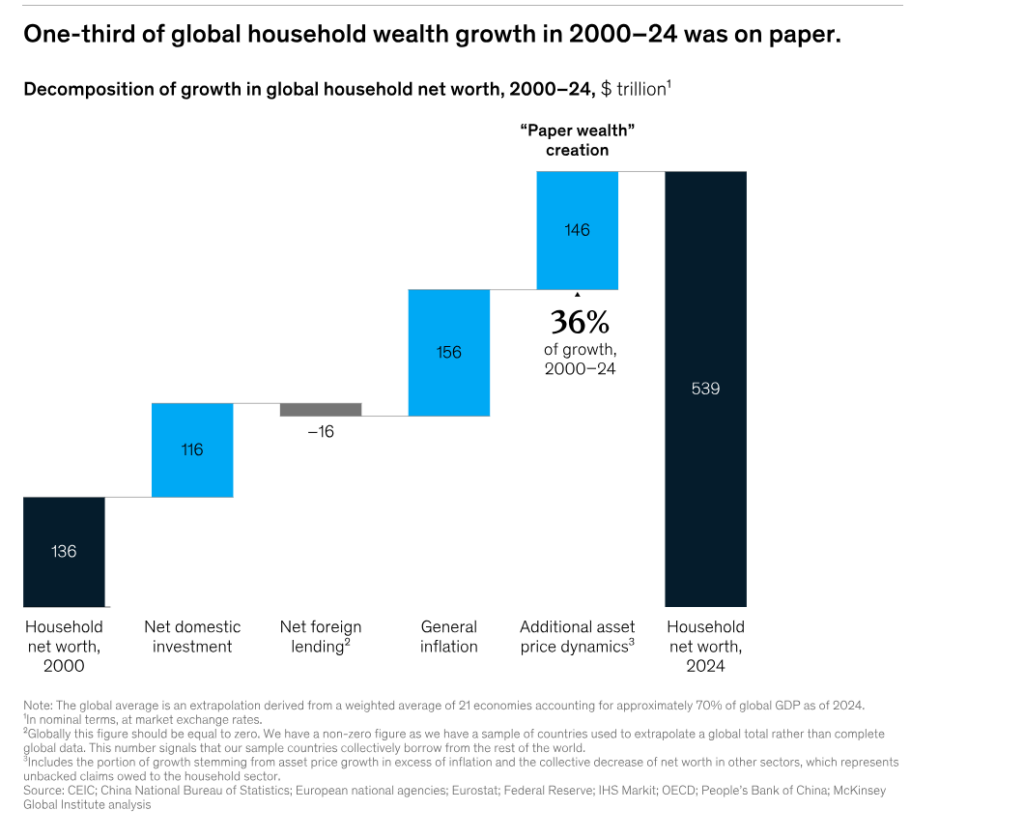

Societal disconnects are real. A McKinsey estimate suggests roughly $146 trillion of “paper wealth” has been created as equity and property valuations pulled away from GDP [1]. Over the past two decades, global wealth has grown much faster than the real economy, driven more by asset price inflation and leverage than by productive investment. (Productivity gains from AI are not the societal solution).

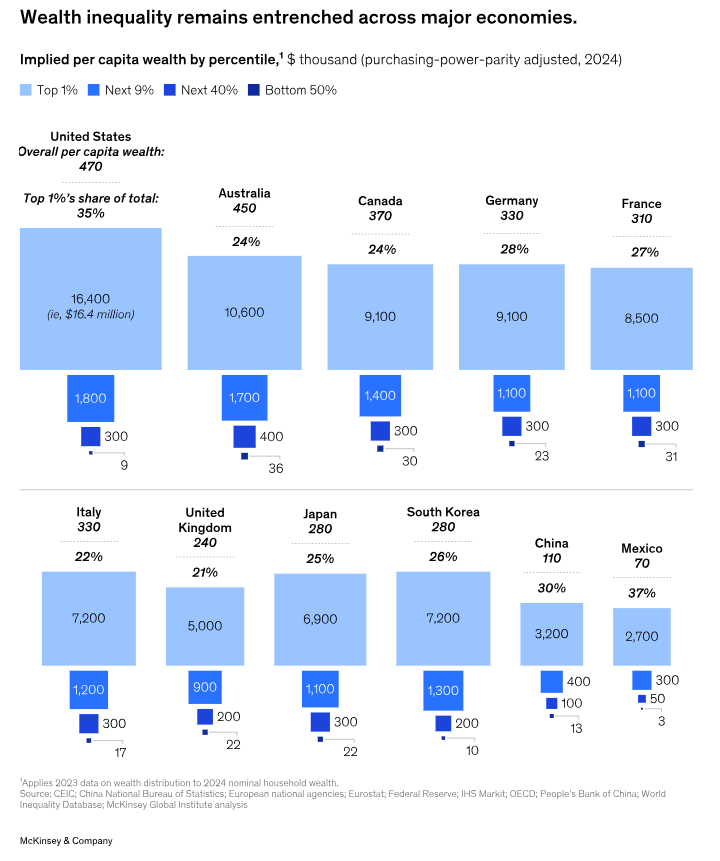

Non-productive investment creates inequality, so those paper gains were also uneven. Owners of assets benefited most; younger households, poorer communities, and many emerging economies benefited least. That imbalance now shows up in populist politics, distrust of elites, and a growing sense that the economic model itself may be broken.

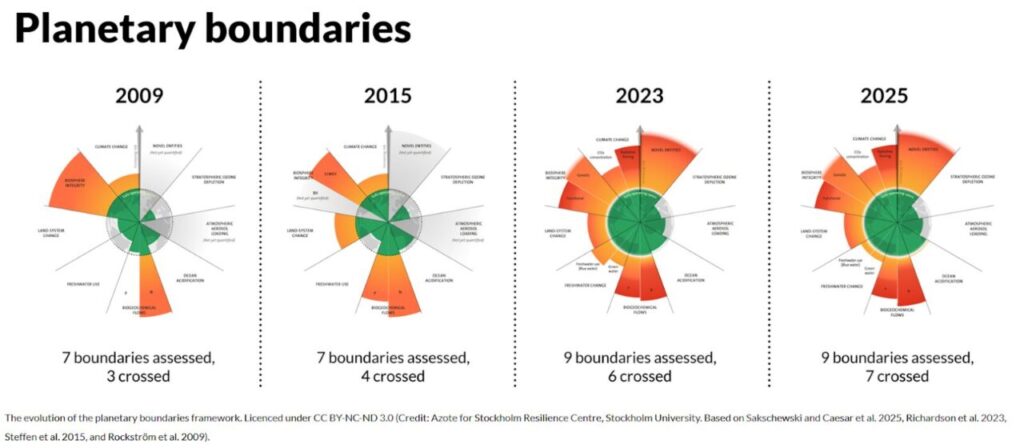

Meanwhile, the planet has been publishing its own balance sheet. The latest assessment from the Stockholm Resilience Centre finds that humanity has already crossed seven of nine planetary boundaries [2]. These are thresholds that define a safe operating space for civilisation. We have become very good at compounding financial claims on the future and very bad at accounting for the physical limits that underpin them.

For all the effort poured into integrating these themes through ESG, the honest answer to many hard client questions is still awkward:

For many investment strategies, ESG factors might not matter enough to investment performance today. We worry they will matter a great deal in the future but that could be beyond the usual performance horizon and even beyond what clients care about. The truth is, we still can’t measure or capture those intangibles very well.

So what ESG was supposed to do (and why it didn’t)

The industry often talks about ESG as if it can do three things at once:

- Protect returns

- Improve real-world outcomes

- Keep everyone happy — clients, regulators, politicians, NGOs

In practice, we blurred concepts that should never have been treated as interchangeable. When creating objectives it should always be clear that ESG integration is not the same as sustainability.

ESG integration, done properly, is about ex ante inputs. It asks what environmental, social, or governance factors could affect future cashflows and valuations.

Sustainability objectives are different. They are about ex post outcomes. Emissions avoided, ecosystems preserved, communities served. These links are harder to measure and often only visible after the fact.

Some in the industry pretended that these are the same thing, so we confused our clients and ourselves.

Metrics that comfort rather than clarify

Lacking a true industry standard, such as a Bloomberg-style reference for ESG, the industry clung to whatever data it could find: ESG scores, carbon footprints, Paris-aligned labels, and SDG icons.

Many of these reference points are crude, noisy, and sometimes perverse to portfolio outcomes.

- Carbon footprints can encourage divestment rather than supporting credible transitions.

- ESG scores often reward rich countries and large firms for being rich and large, not for managing sustainability well.

- “Paris-aligned” passive funds frequently attach long-dated, complex risks to short-term pricing models and pretend the exercise is precise.

In sovereign bonds, where I’ve spent much of my ESG research, this disconnect becomes stark. World Bank research shows most sovereign ESG scores are highly correlated with national income[3]. Treat them as sustainability measures rather than risk proxies, and capital can flow away from poorer countries that need it most to transition.

That’s the exact opposite of what many sustainability-minded clients believe they’re achieving.

Encouragingly, regulators are starting to take note. The UK’s Sustainability Disclosure Requirements push investment managers toward clearer attribution of outcomes rather than marketing claims alone. It’s a step forward, but one that risks being undermined as regulators lean back on simple metrics like carbon footprints, ESG scores, and Paris-aligned proxies simply because they’re easier to supervise. That approach boxes asset managers into neat reporting templates that look credible but achieve little in practice.

Impact funds quietly reveal the problem

Impact funds deserve credit for pushing measurement of sustainability closer to real-world outcomes. But their very existence raises an awkward question:

If only some funds claim to have impact, what exactly is everyone else doing? Especially when holdings often overlap between impact and non-impact funds?

Every investment leaves a footprint. Buying and selling securities in the open market isn’t a one-way trade: when an impact fund sells to a non-impact fund, the real-world outcome barely changes. The problem isn’t that mainstream funds have no impact; it’s that we rarely measure it, own it, or explain it honestly.

When Risk, Return, and Impact Refuse to Line Up

One reason ESG feels broken is that we insist everything is a “win-win”. You can outperform, de-risk, and save the planet. All at once, with no trade-offs.

Clients can see through this. So, three tensions keep resurfacing.

Short-term returns vs long-term resilience

Years of loose monetary policy have trained investors to believe asset prices can detach from the real world indefinitely. From a sustainability perspective, that belief is dangerous. It encourages us to price around climate risk, inequality, and resource depletion rather than pricing them in.

Planetary limits vs financial models

Most valuation models still treat environmental degradation as an externality or an optional scenario. Think of a mining company valued on decades of extraction in a world where ecological and social limits are already being breached. In theory, models could reflect this through discount rates or terminal value assumptions. In practice, many ESG discussions stop at whether emissions line up with a curve or the company has good reporting.

Global focus vs data bias

Standard ESG frameworks systematically favour richer countries and corporates. Used mechanically, they can starve emerging markets of capital precisely when financing the transition there matters most and has the greatest impact.

That is not just a technical flaw. It is a political and moral one.

The illusion of control

Asset managers also overstate how much control we actually have.

Capital markets are vast. Global equities sit around $95 trillion, debt markets near $300 trillion, derivatives notional far larger still [4]. Even the largest managers are small boats in a very big ocean.

We influence behaviour at the margin, through analysis, voting, engagement but we do not set the rules of the system. Yet clients increasingly expect investors to solve problems that governments are unwilling or unable to tackle.

Finance can support public choices. It cannot replace them.

Why ESG needs better questions, not better labels

So where does this leave us?

ESG is not dead. The demand is real, rooted in genuine economic and planetary pressures. But the current toolkit leans too heavily on noisy scores, simplistic labels, and comforting narratives that avoid trade‑offs.

The planet is not waiting for our frameworks to mature. Crossing seven planetary boundaries is not a marketing theme. It is a warning that we are mispricing risk at scale.

In Part 2, I’ll explore what a more honest approach could look like: one that accepts uncertainty, confronts trade-offs, and treats real-world outcomes as central rather than decorative. Most importantly without pretending finance can fix everything on its own.

For now, the diagnosis is simple:

ESG didn’t fail because clients asked the wrong questions. It failed because we gave them answers that were too easy.

[1] https://www.mckinsey.com/mgi/our-research/out-of-balance-whats-next-for-growth-wealth-and-debt

[2] https://www.stockholmresilience.org/research/planetary-boundaries.html

[3] https://documents1.worldbank.org/curated/en/842671621238316887/pdf/Demystifying-Sovereign-ESG.pdf

[4] All of the World’s Money and Markets in One Visualization (2022)

Scott Petrie, CFA, is an experienced sustainable finance expert with 15+ years in asset management and insurance, including roles at Baillie Gifford and T. Rowe Price. Contact Scott at petriescottw@gmail.com

This article was originally published on Medium on February 12, 2026.