The global green bond market started as a niche instrument used mostly by multilateral development banks. It is now one of the primary channels through which institutional capital flows toward climate infrastructure, renewable energy, and sustainable development. But growth has not automatically produced credibility. The bigger the market gets, the harder investors look at who is issuing, what the proceeds actually finance, and whether the label on the bond means anything at all.

I recently spoke with Jamie Friedland, a sustainability analyst at AXA Investment Managers (now part of BNP Paribas Group), about how one of the world’s largest asset managers approaches this question in practice. The conversation surfaced something that gets lost in headline figures about green bond issuance: the gap between what a bond is labeled and what it actually does.

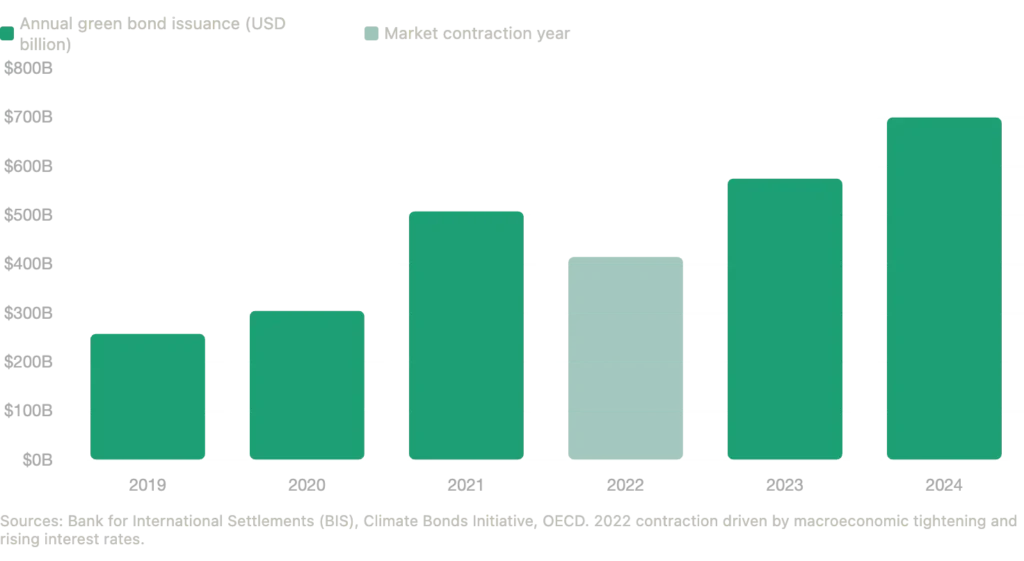

Annual green bond issuance grew from $257 billion in 2019 to approximately $700 billion in 2024, according to data from the Bank for International Settlements.

A Market That Grew Fast and Now Has to Prove Itself

The numbers are hard to ignore. According to the World Bank, cumulative labeled sustainable bonds, covering green, social, sustainability, sustainability-linked, and transition instruments, reached $6.2 trillion globally by the end of 2024. Green bonds account for the largest share of that total, at roughly 57% of all cumulative labeled issuance. Annual green bond issuance alone reached approximately $700 billion in 2024, according to the Bank for International Settlements (BIS).

That growth has forced clarity on terminology. Under the framework set out by the International Capital Market Association (ICMA), green bonds are strictly defined as debt instruments where the proceeds go exclusively toward eligible environmental projects, such as renewable energy or energy efficiency upgrades. Social bonds follow the same “use of proceeds” logic but target social outcomes: affordable housing, healthcare access, food security. Sustainability bonds combine the two. Sustainability-linked bonds (SLBs) work differently. They do not ring-fence proceeds for specific projects. Instead, they are performance instruments where the financial terms, including the coupon rate, can shift depending on whether the issuer hits pre-defined sustainability targets.

These distinctions matter because they determine what kind of accountability an investor can actually expect.

What the ICMA Principles Actually Require

The foundation of the green bond market is the ICMA Green Bond Principles, a voluntary set of guidelines that most major issuers reference. The framework has four core components.

First, Use of Proceeds: funds must go strictly to eligible green projects with clear environmental benefits. Second, Process for Project Evaluation and Selection: issuers must communicate their environmental sustainability objectives and how they select projects. Third, Management of Proceeds: net proceeds must be tracked and properly segregated, not absorbed into general corporate spending. Fourth, Reporting: issuers are expected to publish annual updates on where funds have been allocated, including both qualitative and quantitative performance data, until full allocation is complete.

The framework has worked reasonably well as a market-building tool. The problem is that “voluntary” creates real variation in how seriously different issuers treat these requirements. Some publish thorough post-issuance reports with granular project data. Others treat the label as a marketing exercise and do very little once the bond is sold.

The EU Green Bond Standard Takes It Further

Recognizing that voluntary guidelines have limits, European regulators developed the European Union Green Bond Standard (EU GBS), which became applicable in December 2024. This is a more prescriptive framework than ICMA, and the differences are significant.

Under the EU GBS, at least 85% of proceeds must be invested in activities aligned with the EU Taxonomy for Sustainable Activities, which is the European classification system defining what counts as an environmentally sustainable economic activity. Issuers cannot simply self-certify. External reviewers must be formally registered with and supervised by the European Securities and Markets Authority (ESMA), turning what was previously a reputational exercise into a matter of legal compliance. Issuers who misrepresent their bonds can face administrative or criminal sanctions, something that simply does not exist under ICMA.

This is a meaningful shift. The voluntary market has always relied on reputational incentives to maintain quality. The EU GBS replaces that with regulatory teeth.

Who Gets Rejected and Why

Even under the current voluntary framework, not every bond that claims to be green gets treated as one by sophisticated institutional investors.

The Climate Bonds Initiative (CBI) maintains its own database and actively screens issuances for environmental ambition and transparency. In 2022, the CBI rejected 25% of green bonds from its database, meaning one in every four dollars of labeled issuance failed to meet basic quality thresholds, according to Capital Monitor.

At AXA, Friedland described a structured review process where every use-of-proceeds bond gets a qualitative assessment before it can enter the firm’s green bond strategies. Bonds receive a positive, neutral, or negative opinion. Only those rated positive or neutral are eligible. About 30% of bonds reviewed receive a negative opinion and are excluded.

The most common reasons for rejection fall into a few categories. The first is weak impact reporting. Some issuers commit to publishing post-issuance reports and never do. AXA reviews bonds approximately 18 to 24 months after issuance specifically to check whether that report was published. If it was not, the opinion changes to negative retroactively. The second is problematic use of proceeds. Certain projects that technically qualify under some frameworks do not meet AXA’s stricter internal thresholds. Green building certifications are one example where AXA applies a higher standard than the EU Taxonomy requires. The third is issuer-level sustainability profile. A heavily coal-dependent company issuing a green bond for one transitional project will still fail the review, because the overall profile of the issuer does not align with the stated purpose of the instrument. As Friedland put it, the issuer’s sustainability ambition needs to match the greenness of the bond they are trying to sell.

High-profile greenwashing cases illustrate why this scrutiny matters. Brazilian meat processor JBS faced a formal complaint to the US Securities and Exchange Commission (SEC) over $3.2 billion in sustainability-linked bonds, with critics arguing that the performance targets excluded 97% of the company’s total carbon footprint, while absolute emissions were actually rising, according to reporting by CWR. Other entities, including Anglian Water and TotalEnergies, have faced public and regulatory scrutiny for misleading sustainability claims in recent years.

Institutional green bond review processes often involve post-issuance checks 18 to 24 months after a bond is issued to confirm that promised impact reports were actually published.

The Nuclear Question

One of the more revealing details in the conversation with Friedland was the firm’s treatment of nuclear energy in its green bond strategies. AXA does not include nuclear energy as an eligible use of proceeds in its dedicated green bond funds, even though the EU Taxonomy formally classifies nuclear as a transitional activity.

In September 2025, the EU General Court dismissed a legal challenge brought by Austria against that classification, formally cementing nuclear’s place within the European sustainable finance framework. Despite this, AXA’s green bond strategies continue to exclude it, and the reason is client preference. European investors, who represent the majority of AXA’s client base, have been consistent in saying they do not want nuclear energy included as an eligible project.

This is a useful window into how ESG policy actually gets made inside large asset managers. It is not just about regulatory frameworks. It reflects what clients are willing to accept, which is shaped by factors ranging from nuclear accident history to unresolved questions about radioactive waste disposal. As Friedland noted, this stance may evolve. The defense sector is a recent example of a category that shifted from broadly excluded to broadly accepted within European sustainable portfolios after the geopolitical calculus changed. Nuclear may follow a similar path, but it has not yet.

To be clear: AXA does invest in nuclear energy through conventional mandates. It also holds green bonds issued by nuclear-adjacent companies in its non-green bond strategies, where those bonds are treated as conventional rather than green. The exclusion applies specifically to funds marketed as green bond strategies.

Impact Reporting: Where Things Still Fall Apart

Post-issuance impact reporting remains the weakest link in the green bond market. High-quality supranational issuers like the World Bank and the International Finance Corporation (IFC) consistently publish detailed, project-level reports showing exactly where proceeds went and what the environmental outcomes were. The World Bank’s FY2023 impact report is a reasonable benchmark for what good reporting looks like.

Broader market practice is less consistent. BIS research notes that early green bond issuances carried very little actionable information about actual emissions trajectories, and while the market has improved, there are no binding contractual requirements forcing issuers to demonstrate that their emissions actually declined after a green bond was issued. The EU GBS is attempting to close this gap through mandatory external audits, but this only applies to bonds issued under that specific label.

For investors without robust internal review processes, this remains a real vulnerability. The label on the bond is only a starting point.

How Institutional Investors Fill the Gaps

To address coverage gaps, firms like AXA have built proprietary scoring systems on top of external data providers. MSCI provides the backbone for ESG scoring across more than 17,000 issuers, covering roughly 98 of the world’s top 100 asset managers. But MSCI’s universe does not cover every investment-eligible entity. In markets like US high yield, the benchmark index is only about 70% scored by MSCI. AXA’s analysts cover the remaining 30% through qualitative internal review, assigning scores on the same 0 to 10 scale so that every potential investment has a comparable rating.

Independent third-party verification services also play a role. Second Party Opinions (SPOs) from providers like Sustainalytics, ISS ESG, and S&P Global Ratings are now standard for most large green bond issuances. S&P Global’s acquisition of CICERO Shades of Green in 2022 brought the well-regarded “Shades of Green” methodology into its SPO offering, which grades projects from dark green (pure low-carbon projects) through to red (activities incompatible with climate goals).

None of this eliminates the fundamental challenge, which is that the green bond market still lacks a single, universally binding definition of what qualifies. The EU GBS is the most serious attempt to impose one, but it applies only to issuers who choose to use that label. Most of the market will continue operating under ICMA’s voluntary principles for the foreseeable future. That means credibility depends, in large part, on the rigor of whoever is doing the buying.

Third-party verification providers such as Sustainalytics and S&P Global Ratings now offer Second Party Opinions (SPOs) on most major green bond issuances, adding an independent layer of quality assessment before a bond reaches investors.

You can listen to the full conversation here. For more conversations with institutional investors navigating sustainable finance, visit the SRI 360 podcast.